Reduce Income Tax Bill Via Pension Contributions – Business Owners 2025

What are the pension tax relief limits for my contributions?

The pension tax relief limits for business owners vary depending on the type of company you run.

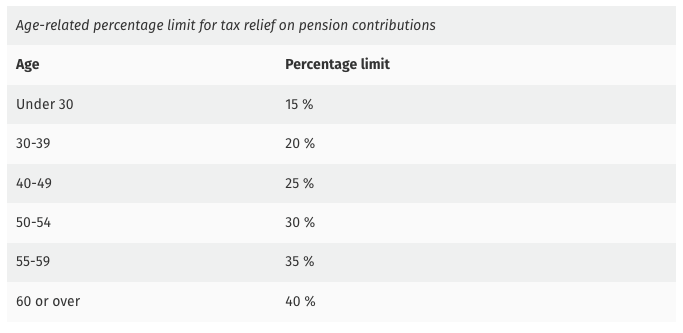

Self-Employed or Sole Trader: If you’re self-employed, your personal pension contributions (to a PRSA or personal pension) qualify for tax relief based on your earnings, but subject to the €115,000 earnings cap.

For contributions made in 2025 but allocated against 2024 earnings, a cap of €115,000 on earnings is in place for tax relief considerations regarding total contributions.

This applies to contributions made to PRSAs, personal pensions, and employee/AVC contributions to company pension schemes.

Note:

- When backdating contributions to 2024, employer PRSA contributions are counted within the specified limits mentioned above.

- The earnings cap does not affect employer company pension contributions.

- In the case of company pension schemes, the combined contributions (employer, employee, and AVC) must adhere to the overall maximum limits set by the Revenue.

Limited Company Owner: If you own a limited company, your personal contributions are also subject to the €115,000 cap, but employer contributions (made by your company) are more flexible and aren’t capped in the same way, offering better tax efficiency.

Transferring Company Profits into a Pension

Transferring company profits into a pension plan offers significant tax advantages compared to conventional profit extraction methods. While taking dividends, purchasing personal assets like cars, or selling your business can result in high tax rates—up to 40% for dividends, 30% for Benefit in Kind, and 33% for Capital Gains and Capital Acquisitions Taxes—contributing to a company pension avoids these costs.

With no Benefit in Kind (BIK) to the employer, corporation tax relief on contributions, and a pension that grows tax-free, this strategy is both efficient and rewarding.

Plus, at retirement, you can access a 25% tax-free lump sum and potentially start drawing from your pension as early as age 50.