A Guide for Business Owners on Protecting, Extracting, and Growing Wealth in Ireland

Tax-Efficient Wealth Extraction Strategies

Extracting wealth from a business requires strategic planning, leading owners to carefully consider and explore the various options available to them.

Conventional wealth extraction methods may not always be the most tax-efficient. Methods such as salaries, dividends, and profits, while common, can incur substantial tax burdens.

To enhance tax efficiency, you should explore alternative wealth extraction strategies, potentially involving pension contributions, tax credits, and deductions.

You can consult with our financial advisors at True Wealth to tailor solutions that align with your financial goals and minimise tax liabilities.

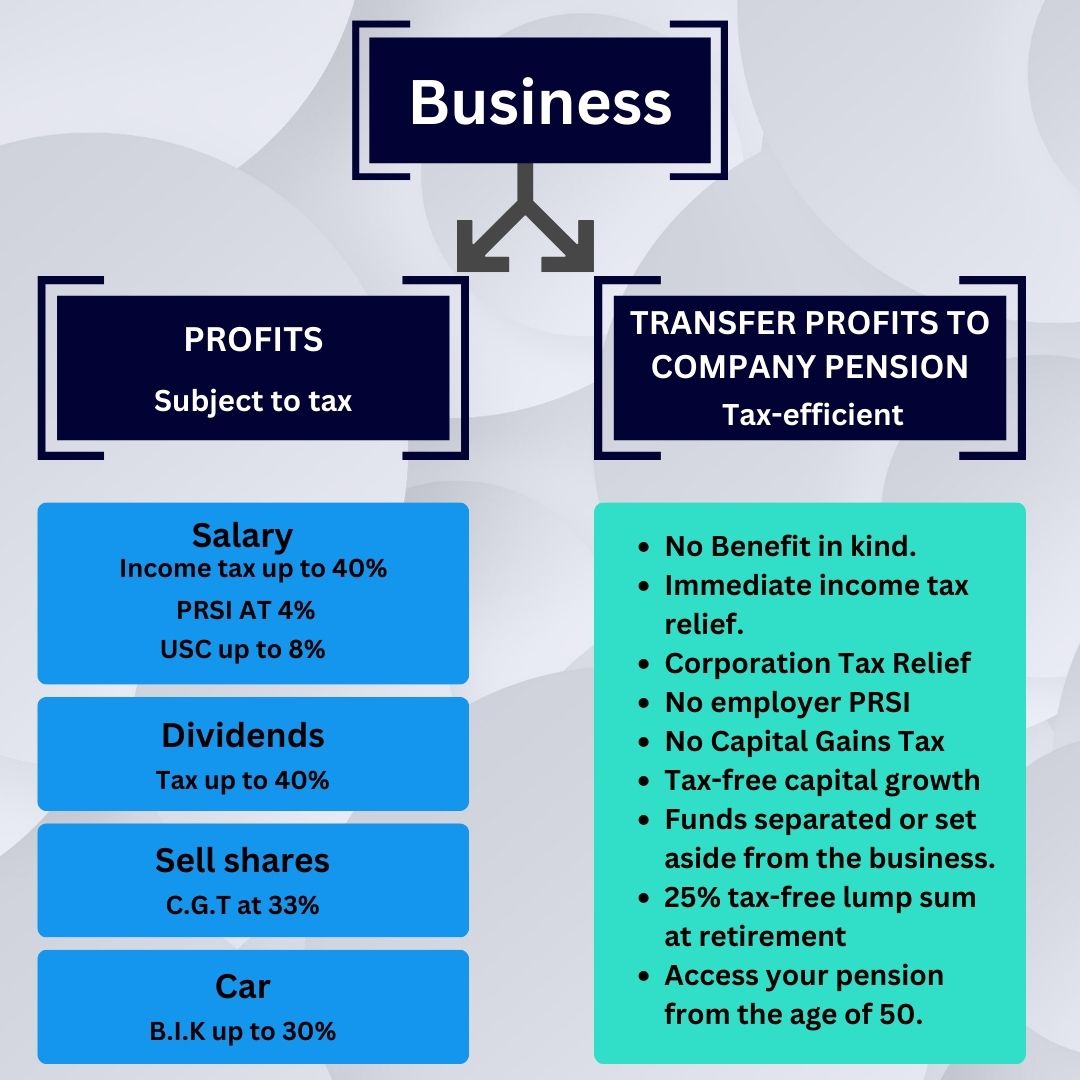

Receiving Salary

Wages and salaries are a typical way to obtain revenue from your company. However, taking income as a salary you may be subject to pay income tax, Universal Social Charge (USC), and Pay Related Social Insurance (PRSI) at rates that can reach up to 52%.

Transferring Company Profits into a Pension

Profits is another traditional extraction method that could lead to higher costs:

Opting for conventional ways to extract profits from your company may seem familiar, but they come with a higher tax burden:

- Taking profits as dividends might result in a tax rate of up to 52%, including PRSI and USC.

- Using the funds to purchase a car for personal use incurs a Benefit in Kind tax of up to 30% of the Open Market Value.

- When selling your company, Capital Gains Tax at a rate of 33% applies.

- In the unfortunate event of death, Capital Acquisitions Tax at a rate of up to 33% is applicable.

Directors will be immediately liable for taxes if they use company profits as their remuneration.

On the other hand, transferring these profits into a company pension plan can be advantageous because:

- No Benefit in kind (BIK) to the employer

- Immediate deduction from income taxes on AVCs and employee contributions

- Corporation tax relief on employer contributions in the year of the contribution is made

- No employer PRSI

- No Capital Gains Tax

- No Corporation Tax

- A pension grows tax-free

- 25% tax-free lump sum at retirement

- You might access your pension from the age of 50

Corporate investments: Can you invest money from your company?