Starting in 2026, all employers will be required to auto-enrol eligible employees into a pension scheme. We help Irish SMEs, company directors, and business owners navigate this change with tailored advice, cost strategies, and compliance support.

Assess the financial impact of Auto-Enrolment on your business.

Compare the State scheme with private pension alternatives.

Set up or upgrade a compliant occupational pension scheme.

Maximise corporate tax relief on employer contributions.

Auto-Enrolment (AE) is a new mandatory retirement savings scheme for employees in Ireland. Applies to workers aged 23–60, earning more than €20,000 per year, who are not already in a pension. Both employee and employer contribute, plus a Government top-up. Contributions are collected by the National Automatic Enrolment Retirement Savings Authority (NAERSA).

Eligible employees will be automatically enrolled by the State system (NAERSA). Employers must match employee contributions and process them through payroll, with the Government adding a top-up. While this creates a new cost and compliance obligation, offering your own company pension scheme can exempt you from AE, and often provides better tax efficiency and flexibility for staff.

How True Wealth Helps Employers

Assess your business impact: Calculate future contribution costs for your staff.

Compare options: Keep the state AE scheme vs. set up your own pension plan.

Plan for compliance: Ensure payroll systems and contracts are updated.

Tax efficiency: Structure contributions to maximise corporate tax relief.

Employee communications: Help explain AE to your workforce.

While Auto-Enrolment is a strong starting point, particularly for younger or lower earners, it may not always be the most efficient choice over the long term. Private pensions (such as PRSAs or company schemes) offer more flexibility: the ability to increase contributions beyond the AE limits, access a broader range of funds, and benefit from higher tax relief (40%) once you move into the higher tax bracket.

This means that while AE helps people begin saving, many individuals, especially as their income grows, may eventually choose to transition into a private pension. Doing so allows them to maximise tax efficiency and build a larger retirement fund over time.

Let’s take Mary as an example. She starts in Auto-Enrolment (AE) at age 26, earning €35,000 per year. By the time she reaches age 40, her AE pension pot could grow to around €43,000.

Now, at 40, Mary’s salary has risen to €60,000. At this income level, switching to a private pension offers a significant advantage. She can claim up to 40% tax relief on her contributions. If she contributes around 15% of her salary into a private pension, her pot could grow to an additional €483,000 by retirement.

Combined with the early AE savings, Mary could retire at 66 with a total pension pot of approximately €636,000. That’s the power of making a smart switch at the right time, maximising tax relief and building long-term wealth.

This shows why having a Financial Planning partner is essential. With the right strategy, you can adapt your pension planning to your career stage and income growth, ensuring you’re not just saving, you’re maximising your retirement security.

Retirement Planning Process

Step 1

Quote & Discovery

Our quote application will gather some vital information to help us understand your current retirement plan and goals. This will include a review of your personal and business income(if applicable), expenses, assets & liabilities alongside a comprehensive review of your current pension arrangements.

Step 2

Plan & Recommendations

Following our analysis, our expert experienced financial advisors will present and explain your tailored retirement plan, allowing you to visualise your and your business' current financial situation and our proposed recommendations to meet your goals within a realistic timeframe.

Step 3

Implement your RETIREMENT plan

Any proposed recommendations can be activated by our dedicated administration team upon your approval. All paperwork can be done online for your convenience and you will be kept informed every step of the way.

Step 4

Ongoing relationship

As part of our service offering, we will consistently review your pension in order to fully realise your personal or business goals. This will involve regular engagement and contact to ensure your pension plan(s) are meeting your current requirements.

PEOPLE ALSO ASK

Auto Enrolment Explained

Who needs to be enrolled?

Employees between the ages of 23 and 60, earning more than €20,000 per year, will be automatically enrolled if they don’t already have a qualifying pension scheme through payroll. This means that many businesses will need to start contributing to staff who previously had no pension arrangements in place. For younger workers under 23 or those earning below €20,000, enrolment will not be automatic, but they will still have the option to join if they wish. Employers should be aware that payroll software will need to capture these thresholds and apply contributions correctly.

How much will it cost my business?

Employer contributions will start at 1.5% of gross pay in 2025 and gradually rise to 6% by 2034. For example, if an employee earns €30,000, the employer contribution will begin at €450 per year and eventually rise to €1,800 per year once the full 6% applies. While this is a new cost for many businesses, it’s important to note that the State will also be contributing to employee pensions, making the scheme more attractive to staff without adding extra expense to employers. Preparing budgets now and forecasting the impact of rising contribution rates over time is key to avoiding surprises.

What if my business already offers a pension scheme?

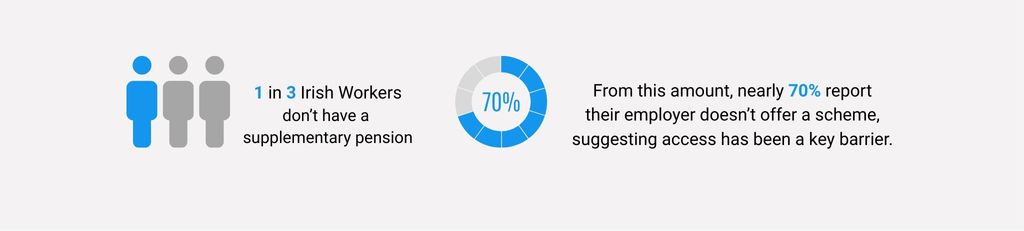

If you already run a payroll-deducted company pension scheme that meets the minimum AE standards, your staff will not be auto-enrolled into the State scheme. This is good news for employers who already invest in pensions, as it avoids duplication. However, businesses that rely on employees paying into private pensions outside payroll will still see those staff auto-enrolled, potentially leading to multiple schemes running at once. Reviewing your existing pension arrangements with a broker can ensure your company scheme remains competitive and positioned as the smarter long-term option for staff.

Can employees opt out?

Yes, employees can opt out, but only during specific windows, such as months 7–8 after enrolment. If they opt out, they will be automatically re-enrolled every two years unless they are in another qualifying pension scheme. Employers should prepare for some administration around opt-outs and re-enrolments, especially for larger workforces. It’s worth communicating clearly with employees upfront to reduce confusion and avoid frustration when these windows open.

Will auto-enrolment replace my company pension scheme?

No. Employers are free to continue offering their own pension scheme, which is often more flexible and provides higher contribution rates, investment choice, and better tax relief. Many companies will position their pension as a benefit that goes beyond the State-backed scheme, helping to attract and retain talent. For example, offering a scheme where the employer contributes 10% rather than the AE minimum 6% can be a powerful recruitment tool. This means auto-enrolment doesn’t have to be the ceiling; it can be the floor on which you build a stronger employee benefits package.

What happens for part-time or seasonal staff?

Auto-Enrolment doesn’t just apply to full-time workers. If you’re part-time, you’ll still be included if you meet certain conditions.

Anyone aged 20 to 60 who earns €20,000 or more per year (combined income) will be automatically enrolled. For example, if you work two part-time jobs and together they bring you over the €20,000 threshold, you will be enrolled, even if neither job on its own pays that amount.

For seasonal or casual workers, the scheme also applies. If your income history suggests you’ll reach €20,000 (for example, by moving from part-time to full-time), NAERSA will review the last three months of pay to verify. If your earnings indicate you’ll cross the threshold, you’ll also be enrolled.

For employers, this means payroll obligations don’t just stop at full-time contracts. If you have part-time or seasonal staff who meet the criteria, you will also be required to contribute. For employees, it means starting to build retirement savings earlier, regardless of your work pattern.

Can I send employees to a financial broker for advice?

Yes, and this can be a real value-add for employers. Auto-enrolment will be new to many workers, and some may not understand the difference between the State scheme and private options. Giving staff access to a broker or adviser can help them make informed decisions and reduce the number of queries HR or payroll teams will have to handle. Employers who facilitate this kind of support will not only ease their own administrative burden but also boost employee trust and satisfaction.

How can my business prepare now?

The most important step is to review your payroll system to ensure it can handle contributions for auto-enrolment. Next, employers should decide whether to rely on the State scheme or to continue (or introduce) a company pension scheme that provides stronger benefits. Finally, clear communication with staff will be essential: explaining what AE is, how contributions will work, and why a company pension may still be the smarter option. Early preparation will put your business ahead of the curve and help avoid compliance risks.

What our 13,000+ clients have to say

Put a lot of time and energy into resolving my complicated financial requirements. Top class committment and guidance throughout.

An indepth, practical understanding of the current financial market in Ireland and seems well positioned to advise any situation. I highly recommend getting in touch.

I just had the experience I wish I got with every company I deal with, exceeding expectations.

Now I have a better understanding of my finances and I'm able to save more money and plan for the future. She also advised on having a children's savings plan to save for my child’s college education.

PARTNERED WITH

WE CAN ALSO HELP WITH..

Assessing all areas of your finances

And assess areas for potential improvement to help you make data-driven decisions. Pinpointing areas of strength or weakness in your personal finances or business operations.

Discovering your financial goals

We will discuss your personal and business’ goals and visually display them on your personal / business roadmap. Additionally, this will incorporate external factors such as inflation, income raises and interest rates. We can also present “what if” scenarios and the effect it has on your personal or business’ finances over time.

Creating a plan

After we assess your finances we will propose a plan which may include pensions, savings plans, investments or insurance to better assist you in achieving your goals within the agreed timeframe.

Protection Package

Having a comprehensive protection package ensures peace of mind by safeguarding you and your loved ones, shielding against unforeseen expenses throughout your lifetime.

Regular reviews

Financial planning is a life-long process. Reviewing the actions recommended in your plan should take place regularly and in the event of change of income, assets, business or family circumstances. This is something we will be facilitating through our service offering.

Mortgage Assistance

As an experienced mortgage intermediary, we can help you on all things mortgage-related, including government schemes, designed to help you acquire your dream home. We will provide you with an independent comparison of lenders and mortgage options available as well as manage the entire mortgage process from start to finish.

Our #1 goal is helping you to achieve yours.

Our team of financial advisors take a personalised and holistic approach to retirement planning, creating a tailored retirement plan that meets your unique requirements and goals.

You may also like to explore our articles and stay up-to-date.

What Auto-Enrolment Really Means for Business Owners and Company Directors

Benefits of Offering Pensions to Employees

Auto-Enrolment in Ireland: What It Means for Employees

Business Owners’ Guide to Master Trust Pensions

Auto-Enrolment: Key Questions Answered for Business Owners

What Are the Differences Between a State Pension and a Private Pension?

True Financial Freedom made easy.

Subscribe to our YouTube Channel.

Subscribe to our YouTube Channel and explore our insights and tips, empowering you to make informed decisions that will not only protect your future and loved ones, while also ensuring you achieve all your financial goals.