Additional Voluntary Contributions (AVCs) are optional payments that individuals can make to supplement their pension savings beyond the regular contributions to their workplace or personal pension scheme. The advantages of AVCs lie in the flexibility they offer. By contributing additional funds, individuals have the opportunity to boost their pension pot, providing a financial cushion for retirement. The contributions are typically voluntary, allowing individuals to decide the amount and frequency of payments based on their financial circumstances. Furthermore, AVCs can enhance tax efficiency, as contributions may qualify for tax relief, potentially reducing the overall tax liability. This flexibility and potential for increased retirement income make AVCs a valuable tool for those seeking to optimise their pension planning and ensure a more comfortable retirement.

Since it’s your AVC, you have the flexibility to adjust your contributions—whether increasing, decreasing, stopping, or restarting—at any point. This adaptability allows you to align your AVC contributions with the evolving priorities in your life, ensuring that your investments can grow along with your changing needs. Once you become a member of your employer’s Superannuation Scheme, you become eligible to participate in an AVC Plan. Contributions are subject to the maximum limit set by Revenue, with a minimum monthly contribution of €75 (or equivalent).

Tax relief for PRSA AVCs is determined by the appropriate age-related percentage limit of the income earned from the relevant employment. This limit is adjusted to account for any employee contributions made to the pension scheme associated with that employment.

You have the option to make a one-time or special contribution after the conclusion of a tax year. This contribution must be made before the following 31st of October of the current year.

If you opt to make such a payment, you can choose to receive tax relief for the contributions in the preceding tax year. This adjustment also needs to be completed before the 31st of October in the subsequent year.

It’s important to note that when utilising the Revenue Online Service (ROS), there may be extensions to the deadlines for both contribution payments and making this retroactive tax relief choice.

Don’t wait any longer to start your journey and be prepared financially to retire when you want. Get a quote today!

Many employers in Ireland offer pension schemes as part of their employee benefits package. These pension schemes often include employer contributions. When your employer contributes to your private pension, it’s essentially “free money” that boosts your retirement savings without requiring additional personal contributions. It’s a valuable perk that can significantly enhance your retirement fund.

The tax relief for pension contributions has two primary limitations:

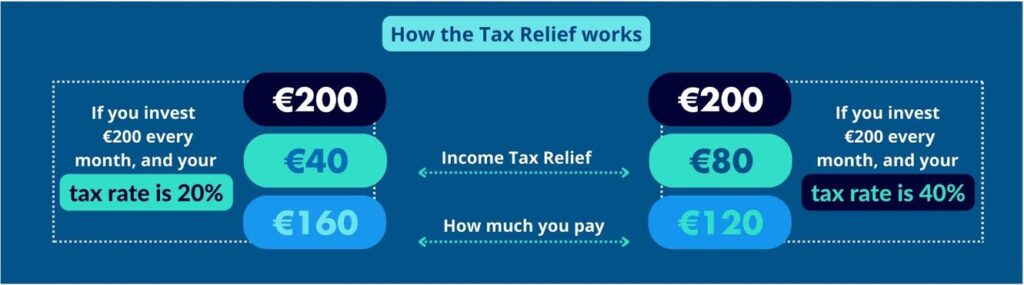

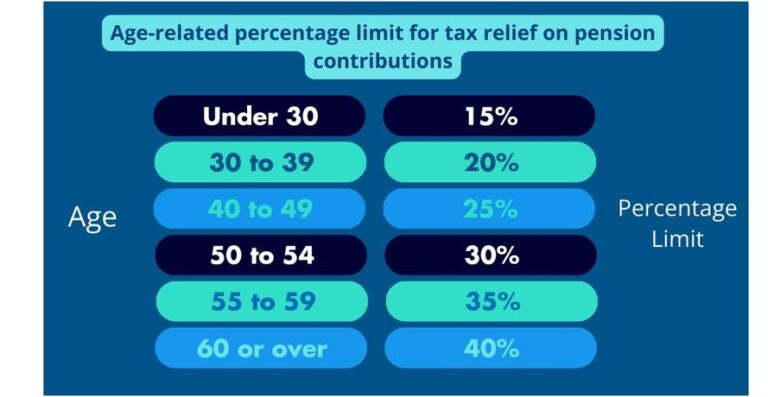

You can receive tax relief up to the applicable age-related percentage limit of your earnings within a given year. For instance, when you’re 29 years old, there’s a limit of 15% of your total income that can be allocated to your pension fund. This allocation limit incrementally increases as you progress through age groups, reaching its highest point at age 60 and beyond, currently standing at 40% of your salary. If you have multiple sources of income, this relief applies solely to the income source for which the contributions are being made.

Total earnings limit

The maximum annual earnings considered for calculating tax relief is €115,000. It’s important to note that employer contributions to an employee’s pension scheme are not factored into the calculation of the employee’s earnings threshold.

Optimise your retirement funds and protect your future. Book your appointment and start now!

Planning for retirement is a significant life milestone. Whether you’re just starting to think about retirement or are already well into your retirement journey, this guide aims to empower you to make informed decisions and create a retirement plan that aligns with your unique financial goals and expectations.

After you download your guide, one of our expert mortgage advisors will be in touch shortly to provide you with guidance and further relevant information.

As awareness of climate change and social responsibility continues to rise, an increasing number of individuals are keen on integrating ethical and sustainable investments, commonly referred to as ESG investing, into their retirement portfolios. There are diverse opportunities for ethical and sustainable investing, including options like green bonds, renewable energy funds, and socially responsible funds. The Aviva Multi-Asset ESG Fund is a great example of the growing interest in ESG investing. It’s a fund designed to give investors a mix of different assets while also considering environmental, social, and governance factors. The goal is to balance making good financial returns with having a positive impact on society and the environment.

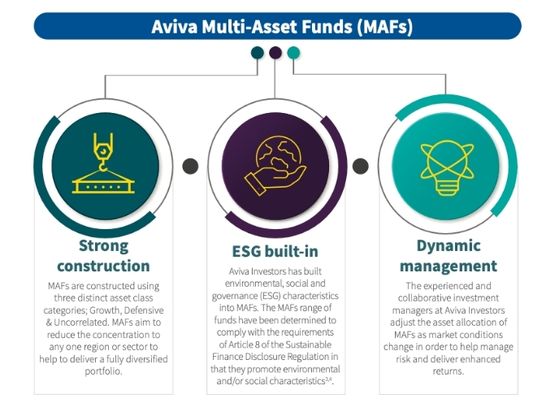

Aviva’s tailored Multi-Asset Funds (MAFs) offer a diverse selection to meet various risk profiles, allowing for transitions to higher or lower risk and reward profiles with assistance from True Wealth. These funds strategically diversify across growth assets (such as equities), defensive assets (like bonds), and uncorrelated assets (including absolute return funds). Aviva’s ESG integration ensures alignment with Article 8 requirements, incorporating environmental and/or social characteristics. With dynamic management, the funds proactively adjust to market dynamics, effectively minimizing risk and optimizing returns. With over €87 billion managed globally and more than 35 years of multi-asset investment experience, Aviva Investors leverage their expertise through a team of over 55 committed professionals, holding about €2.2 billion in assets solely in Ireland.

Aviva Life & Pensions Ireland Dac, trading as Aviva Life & Pensions Ireland and Friends First is regulated by the Central Bank of Ireland.

Warning: Past performance is not a reliable guide to future performance.

Warning: The value of your investment may go down as well as up.

Warning: If you invest in this product you will not have any access to your money until you retire.

Warning: If you invest in this product you may lose some or all of the money you invested.

Warning: This product may be affected by changes in currency exchange rates.

Eight out of ten pension holders are worried about the effects of climate change, per research from Aviva. Through investing in businesses that place a high priority on ethical standards, sustainability, and transparency, people can effectively match their financial decisions with their environmental ideals. Aviva’s ESG initiative customises investments to make a beneficial impact on the environment and society in addition to potential financial gains.

Additionally, you can delve deeper into ethical and sustainable investments by exploring our post:

Yes, in Ireland, you have the flexibility to modify your Additional Voluntary Contributions (AVCs) at your discretion. You can increase, decrease, stop, or restart your AVC contributions as needed. This adaptability allows you to align your pension strategy with changing financial circumstances, ensuring that you have control over the level of contributions based on your preferences, life events, or evolving priorities. Whether you choose to adjust the amount or frequency of your AVC contributions, this flexibility empowers you to tailor your pension planning to best suit your individual needs and financial goals.

Additional Voluntary Contributions (AVCs) becomes particularly advantageous at various stages in your career and life. A good time to contemplate AVCs is when you experience an increase in disposable income or receive a salary boost, as this provides an opportunity to enhance your pension savings. Additionally, major life events such as marriage, the birth of a child, or even a promotion could be opportune moments to reassess and potentially increase your AVC contributions. Furthermore, if you find yourself with surplus income after meeting essential expenses, redirecting those funds towards AVCs can fortify your pension fund for the future. Ultimately, the optimal time to consider AVCs is subjective and depends on individual circumstances, financial goals, and life milestones. Regularly reassessing your situation and consulting with financial advisors can help determine the most strategic times to maximize the benefits of AVCs in your pension planning.

In Ireland, the accessibility of your Additional Voluntary Contributions (AVCs) is typically aligned with the rules governing your main pension scheme. The standard age for accessing both your main pension and AVCs is usually 65, which corresponds to the State Pension Age. However, certain circumstances may allow for earlier access to your AVCs, such as early retirement or ill health. Early retirement may permit access to your AVCs from the age of 50, subject to your main pension scheme rules. It’s essential to review the specific terms and conditions of your pension scheme to understand the criteria for accessing your AVCs and any potential implications on benefits based on your chosen retirement age or circumstances. Seeking guidance from pension administrators or financial advisors is recommended to ensure a clear understanding of the rules governing AVC accessibility in alignment with your unique situation.

Warning: Past performance is not a reliable guide to future performance.

Warning: The value of your investment may go down and up.

Warning: If you invest in this product, you will not have any access to your money until you retire.

Warning: If you invest in this product, you may lose some or all of your investment.

Warning: This product may be affected by changes in currency exchange rates.

Income, Life, Mortgage, Health, Serious Illness Protection

Freephone (1800) 808-808

Unlock your full retirement potential and reach your financial milestones with a tax-efficient pension review guided by our experienced and qualified Financial Advisors. Schedule your consultation today with our award-winning team and set the course for a well-planned financial future enriched by expert Financial Advice.

Make informed decisions. Explore our articles and stay up-to-date.

Subscribe to our YouTube Channel and explore our insights and tips, empowering you to make informed decisions that will not only protect your future and loved ones, while also ensuring you achieve all your financial goals.

At True Wealth, we believe everyone deserves access to expert financial advice, regardless of their current wealth or financial situation. If you have a passion for connecting with people and aspire to thrive in a culture built on trust, integrity, dedication, and excellence, this could be the perfect fit. Let’s grow together!