Favourite Nephew/Niece Relief: Inheritance Plan for Business Owners

Business owners often aim to transfer their business assets to the next generation, typically passing them on to their children for continued family business management.

However, sometimes the most suitable person to take over the company’s operations is a niece or nephew who has been actively involved in the business.

In rural families, especially, there is a notable connection between aunts or uncles and their nieces and nephews. In instances where farmers without children wish to preserve their land within the family, they may consider passing the business on to a niece or nephew as the next of kin.

Certainly, these farmers may also contemplate transferring the farm to their surviving siblings instead of a niece or nephew. From a tax planning perspective, opting for the transfer to a nephew or niece could be more advantageous.

Nephew or Niece Qualification Criteria

In the context of this relief, you qualify as a nephew or niece if you are:

- The child of the disponer’s brother

- The child of the disponer’s sister

- The child of the disponer’s brother’s civil partner

- The child of the disponer’s sister’s civil partner

Eligibility Criteria for the Nephew/Niece Relief

To qualify for the relief, you need to have been employed by the disponer for the five years directly preceding the receipt of the gift or inheritance. During this period, your work commitment should have exceeded either:

- 24 hours per week at the business location, or

- 15 hours per week at the business location, provided that the business is exclusively operated by you and either the disponer or the disponer’s spouse or civil partner.

Note that the relief specifically applies to assets used in the business, with the Group B threshold applicable to non-business assets.

If the gift or inheritance includes both business and non-business things, you have to allocate the liabilities between the two types of assets.

Tax Advantages

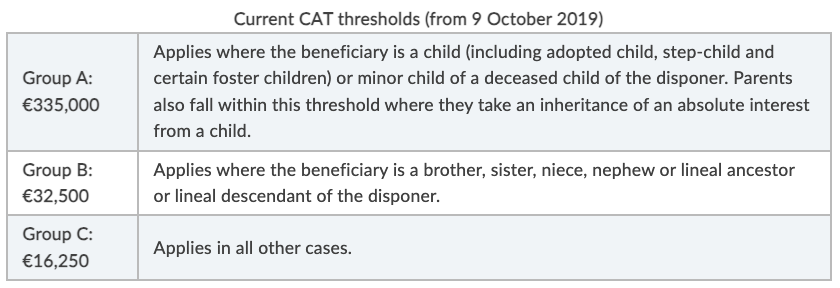

Capital Acquisitions Tax (CAT) is a tax imposed on gifts and inheritances you receive from others, such as family members or friends. The amount of tax you pay depends on the value of the gift or inheritance and your relationship with the person giving it.

There are group thresholds to determine the amount of tax payable. These thresholds vary based on your relationship with the person giving the gift or inheritance. The closer the relationship, the higher the threshold, meaning you can receive a larger amount without paying tax.

Normally, gifts or inheritances between uncles/aunts and nephews/nieces fall into group B, attracting higher tax rates.

The nephew and niece relief enables the use of the Group A threshold, leading to a more advantageous tax treatment.

It’s a much more tax-efficient transfer of assets within the family, preserving wealth for the next generation.

{kind=link}