{kind=link}

Tax-Free Growth Potential

The money within your Retirement Bond has the current advantage of growing tax-free.

This tax advantage provides the potential for accelerated growth compared to other savings plans subject to taxation, contributing to the overall efficiency of your retirement savings strategy.

Consistent Retirement Options

Your retirement options remain consistent with those allowed in your previous scheme.

Whether you prefer a secure income for life, flexible access to funds, a lump sum payment, or leaving your savings invested until needed, a PRB accommodates the same choices.

Full Payout on Death

In the unfortunate event of your death before retirement, the full value of your PRB is paid out to your estate. This feature ensures that your beneficiaries receive the entirety of your PRB’s value upon notification of your passing.

Tax-Free Lump Sum at Retirement

Upon retirement, you have the option to take a portion of your pension fund as a tax-free lump sum, currently subject to a lifetime limit of €200,000.

This financial flexibility provides the opportunity to fulfill long-awaited personal endeavors or indulge in activities you have always envisioned.

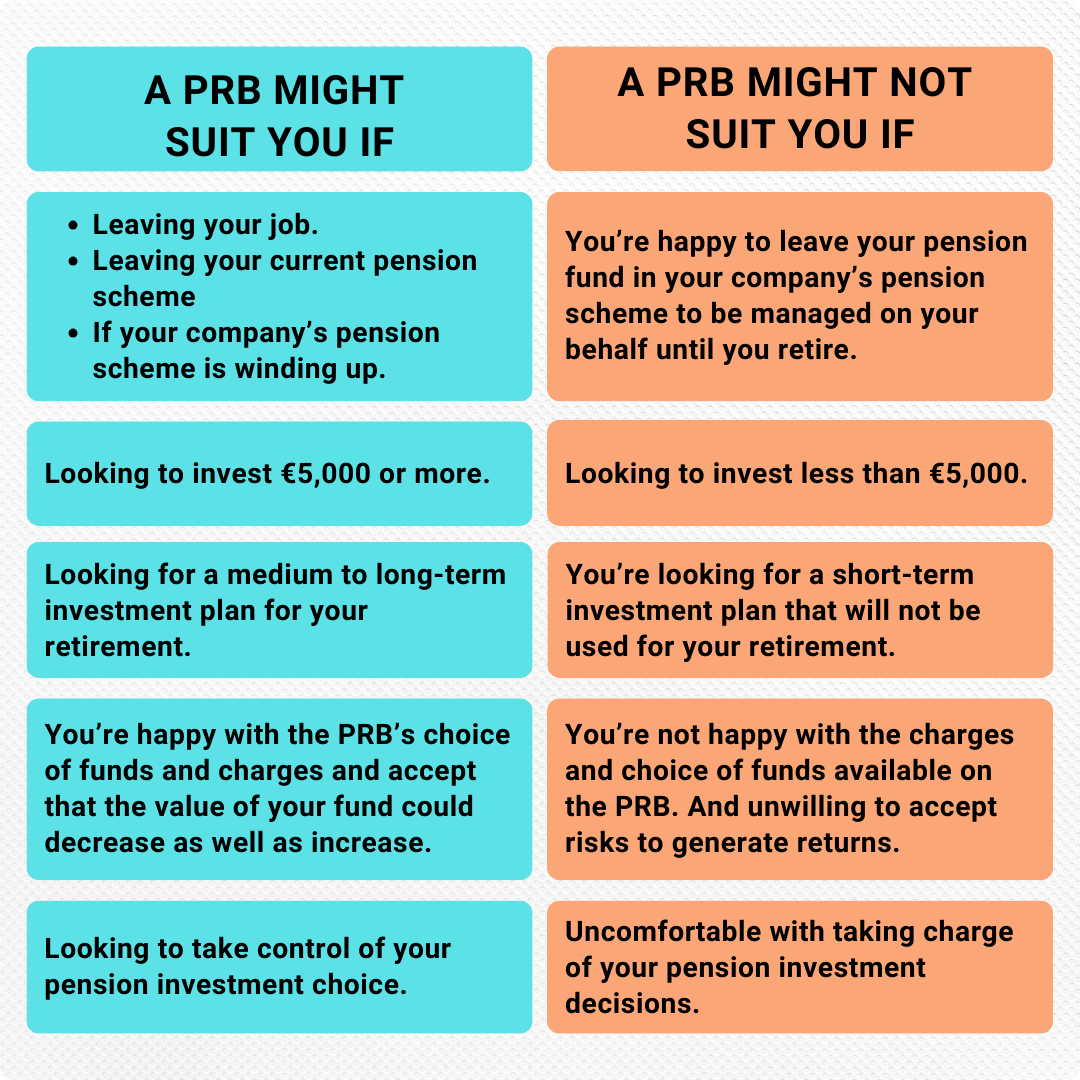

Is a Personal Retirement Bond right for you?

Can I cash in my retirement bond?

You are not allowed to take money out of a Retirement Bond until you are at least 60 years old.

There are two exclusions to this rule: you can retire at any age due to illness, or you can start receiving benefits from your Retirement Bond at age 50 if you have left service.

Retirement Planning in Ireland: Your Comprehensive Guide