Retirement Planning in Ireland: Your Comprehensive Guide

Planning for retirement is a significant life milestone, and ensuring a financially secure and comfortable retirement requires careful consideration and informed decision-making.

This guide will provide you with comprehensive knowledge to help you navigate the complexities of retirement planning and pensions.

Whether you’re just starting to think about retirement or are already well into your retirement journey, this guide aims to empower you with the knowledge needed to make informed decisions and create a retirement plan that aligns with your unique financial goals and expectations.

Why should I start a private pension?

Having a private pension in Ireland is crucial for several reasons, including ensuring a comfortable retirement or maintaining your current lifestyle. Private pensions are also important for:

Supplementing State Pension

Although the State Pension provides retirees with important financial support, it might not be sufficient to maintain your standard of living or cover all your financial needs during retirement.

Consider your bills and expenses you might have during retirement and weigh whether relying solely on the State Pension, which stands at €265 per week as of January 2023, will be enough for your financial security while keeping in mind that you might also like to have a nice standard of living during retirement.

Private pensions bridge the gap between state pensions and financial needs, protect against inflation, and provide peace of mind. They also enable legacy planning, ensuring financial support for loved ones.

Tax benefits

Contributing to a private pension can lead to substantial tax relief, with individuals potentially receiving tax relief of up to 40% on their contributions. This is one of only two financial products that the government will actually pay towards you, the other is income protection.

Additional Benefits

There are several reasons you should start your private pension, such as the possibility of retiring early.

To learn more about other key benefits of having a private pension, read our article, 9 Reasons to Have a Private Pension in Ireland.

When is the best time to start a pension?

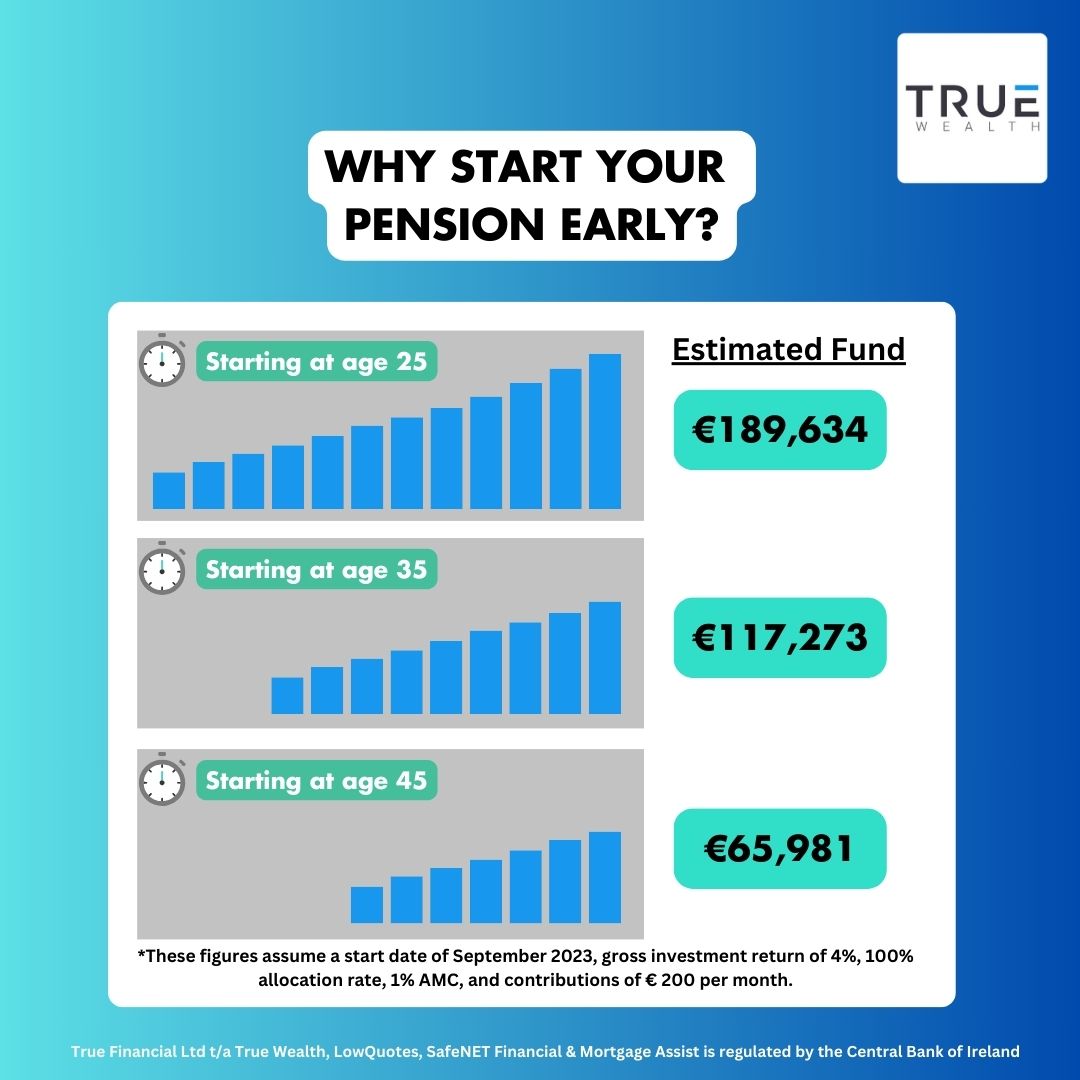

The best time to start a pension is right now. Delaying this crucial financial decision can significantly impact your retirement savings.

Starting as early as possible allows your investments to grow over time, potentially providing you with a more substantial pension fund when you retire.

The power of compound interest and time is on your side, making today the best moment to begin securing your financial future in preparation for retirement.

Explore this graph showing estimated funds at ages 25, 35, and 45.

What is a PRSA pension?

A PRSA (Personal Retirement Savings Account) is a privately owned pension plan that offers flexibility in saving for retirement.

With a PRSA, you have the freedom to make contributions at your convenience and can also choose to discontinue contributions whenever you wish.

Anyone can join a PRSA, regardless of their employment status. Whether you are self-employed or employed by a company, you can establish and maintain a PRSA.

What is a PRB?

A Personal Retirement Bond (PRB) is an individual policy established by pension scheme trustees to secure retirement benefits for a former member of the scheme.

Essentially, if you leave a pension scheme, you have the option to transfer your pension benefits by having the fund’s value invested in a bond.

If you are considering leaving your current employer, especially if you are a member of the group pension plan, a Personal Retirement Bond (PRB) can be an excellent choice.

A PRB is also a suitable option if you opt to leave a company pension scheme for various reasons or if the scheme is in the process of winding down.

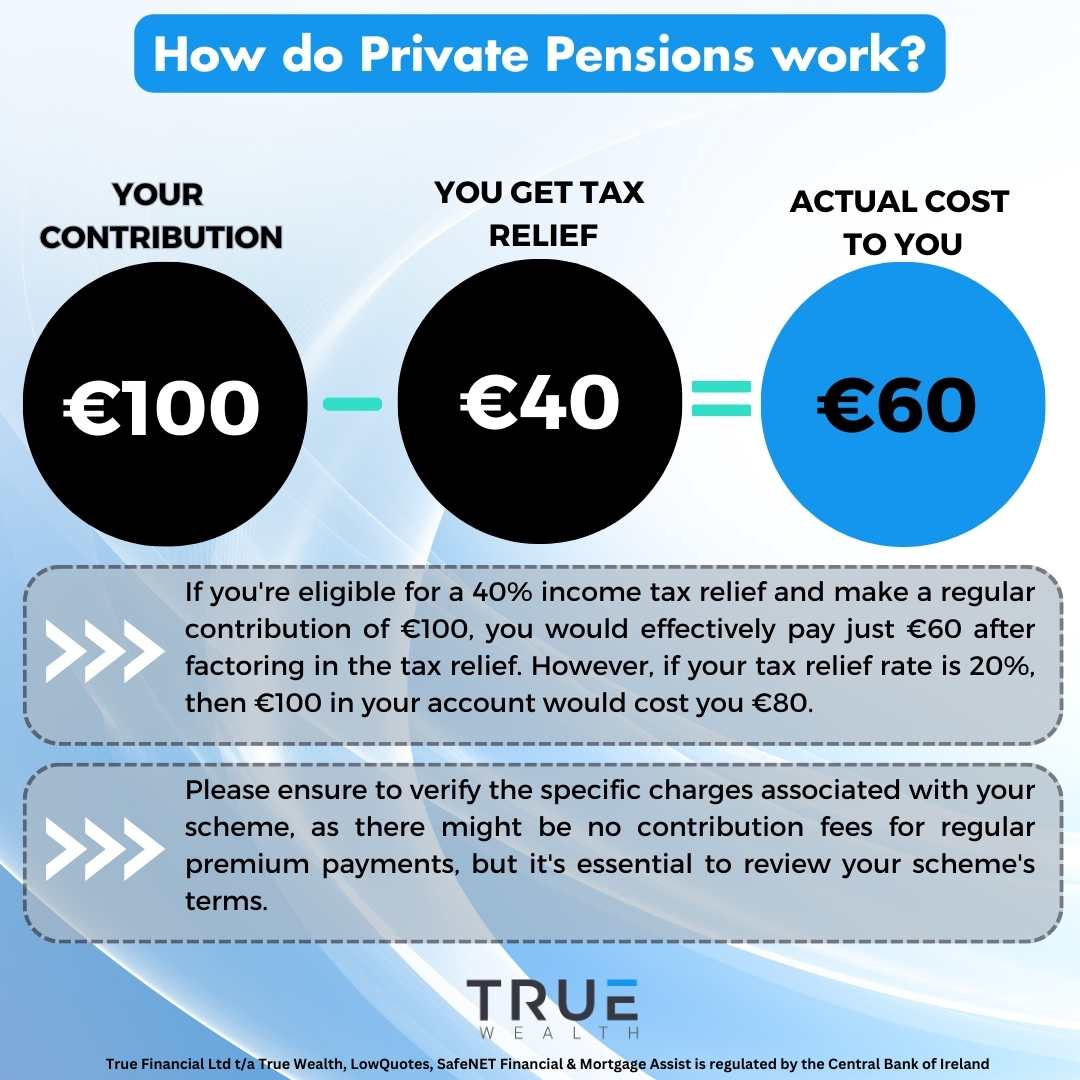

How do private pensions work

When you contribute to your private pension, the government provides tax relief on those contributions.

This means that the money you contribute to your pension is deducted from your taxable income, reducing the amount of income that is subject to taxation.

The level of tax relief you receive depends on your income and the tax rate applicable to you.

For example, if you are in the higher tax bracket and you contribute €1,000 to your private pension, you may receive €400 in tax relief, effectively reducing the cost of your contribution to €600.

This tax relief can significantly boost your retirement savings over time.

Furthermore, a private pension allows you to take control of your retirement savings, offering flexibility in investment choices and providing opportunities for your contributions to grow over the years.

This control empowers you to tailor your pension plan to your specific financial goals and risk tolerance.

How Much Should I Save for Retirement?

Determining how much you should save for retirement involves considering various factors to create a personalised retirement plan. Here are key factors to consider:

Your Desired Lifestyle in Retirement

Think about the type of lifestyle you want to lead during retirement. Consider your housing, travel, leisure activities, and other expenses. This will help you estimate your retirement budget.

Current Age and Retirement Age

Your current age and the age at which you plan to retire are crucial. The sooner you start saving, the more time your investments have to grow. Delaying retirement allows you to save more.

Consider life expectancy

It’s important to note that predicting your exact lifespan and the required duration of your pension is uncertain.

However, we can gain insights by considering the current life expectancy, providing a starting point for planning. From there, you can build and refine your retirement strategy.

With improved health and increased life expectancy among the aging population, life expectancy is on the rise.

By the year 2046, men can anticipate an average lifespan of 85 years, while women can expect to live until around 89 years on average, according to the Central Statistics Office.

Expected Inflation

Consider the impact of inflation on your future expenses. Prices tend to rise over time, so your retirement savings need to keep pace with inflation.

Inflation is the gradual increase in the cost of living over the years. To maintain your purchasing power in retirement, it’s crucial to account for inflation when calculating your retirement savings.

Types of Funds and Risks

The specific funds you select for your retirement savings can greatly impact the potential for compound growth.

Generally, investing in a diversified portfolio of assets can help spread risk and maximise growth potential.

The level of risk you’re comfortable with will depend on your individual financial situation and risk tolerance.

Younger individuals may opt for a more aggressive investment strategy, while those closer to retirement might choose a more conservative approach.

Employer Benefits

If your employer offers a pension plan with matching contributions, take full advantage of it. Employer contributions can significantly boost your retirement savings.

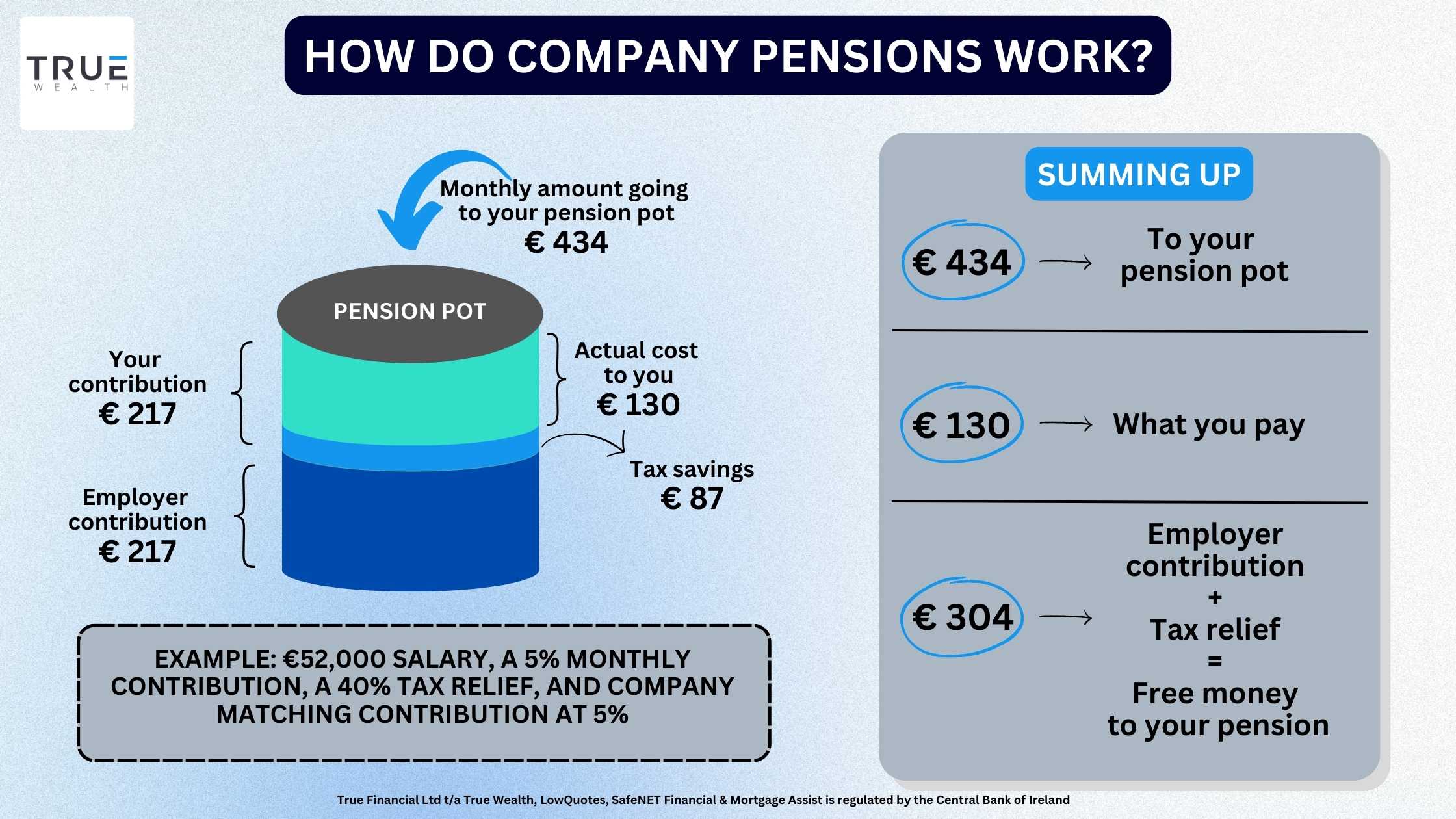

For example, let’s take the scenario where you are an employee and have a company pension plan.

You’re earning €52,000 per year, contributing 5% of your annual salary per month. The company’s contribution matches your contribution at 5%.

Additionally, you fall within the 40% tax bracket.

Both you and your employer are contributing €217.

The crucial point to note is that thanks to tax relief, your effective cost is only €130. This means you’re able to contribute more to your pension pot while paying less, all thanks to the tax relief benefit.

You’re getting €304 more into your pension pot, it’s literally free money!

Use a Pension Calculator

You can also use a pension calculator. This tool can assist you in determining the appropriate amount to allocate to your pension.

Additionally, it will illustrate the potential tax relief you could qualify for on your contributions.

You may quickly determine the suggested retirement savings you should start saving for by entering your personal information and defining your retirement goals.

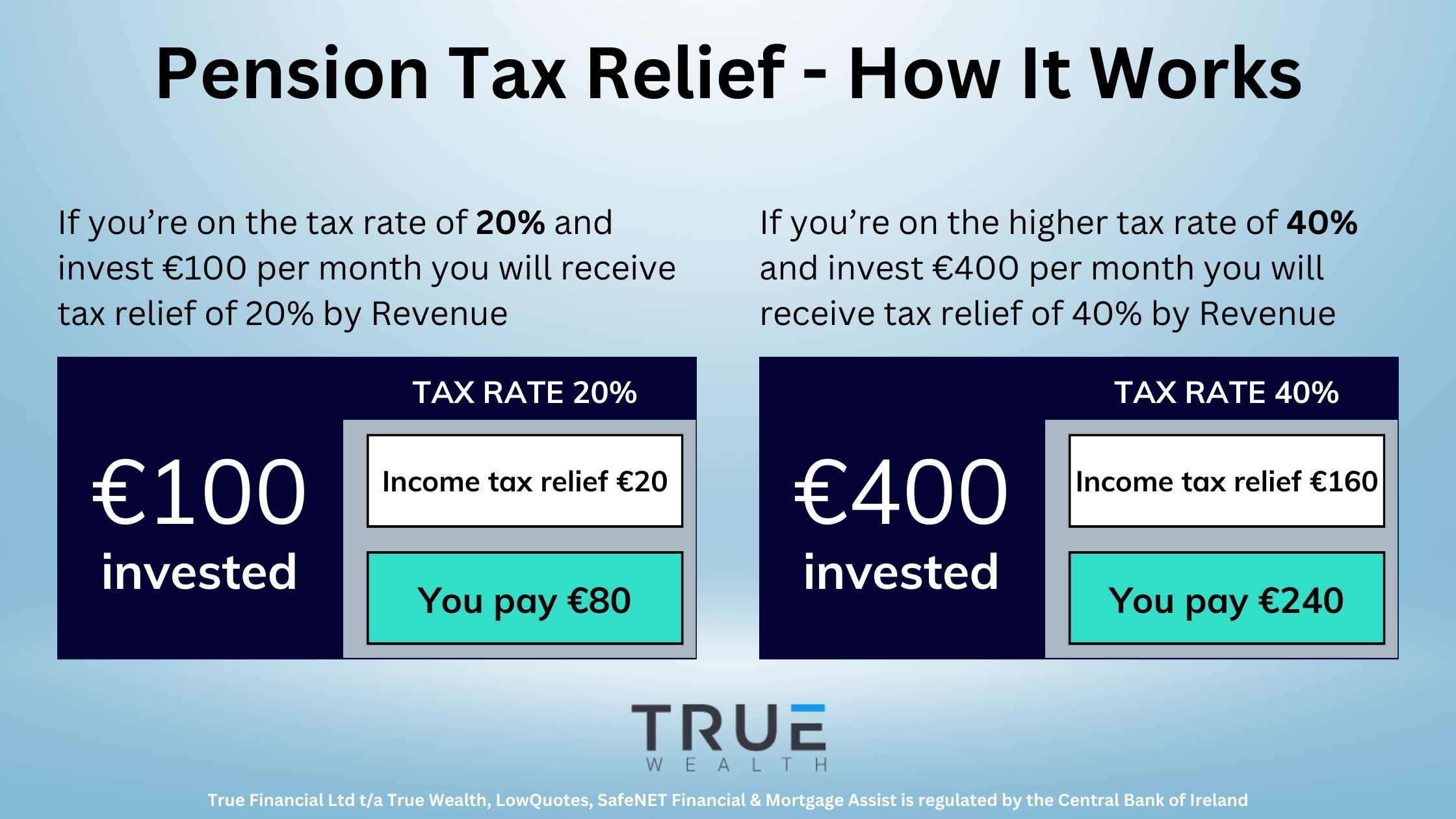

How does tax relief work on pension contributions?

If you contribute to a pension plan, you are eligible to receive an income tax relief on your contributions.

The maximum income tax rate that applies to you, also known as the marginal rate, determines the amount of tax relief on your pension payments.

The exact benefits and rules can vary, so it’s advisable to consult with one of our financial advisors at True Wealth.

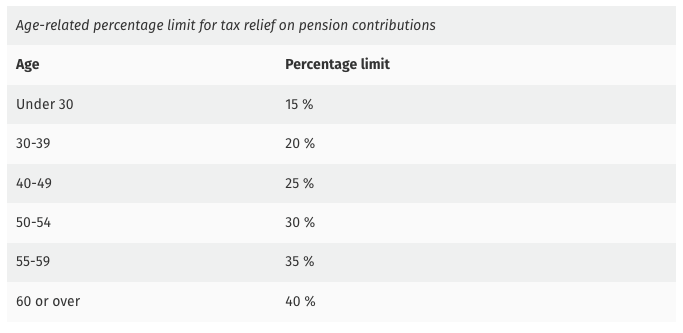

What is the maximum pension contribution amount eligible for tax relief?

The tax relief for pension contributions has two primary limitations:

- An age-related earnings percentage limit.

- A total earnings limit.

Age-related contribution limits

You can receive tax relief up to the applicable age-related percentage limit of your earnings within a given year.

For instance, when you’re 29 years old, there’s a limit of 15% of your total income that can be allocated to your pension fund. This allocation limit incrementally increases as you progress through age groups, reaching its highest point at age 60 and beyond, currently standing at 40% of your salary.

If you have multiple sources of income, this relief is applicable solely to the income source for which the contributions are being made.

Total earnings limit

The maximum annual earnings considered for calculating tax relief is €115,000.

It’s important to note that employer contributions to an employee’s pension scheme are not factored into the calculation of the employee’s earnings threshold.

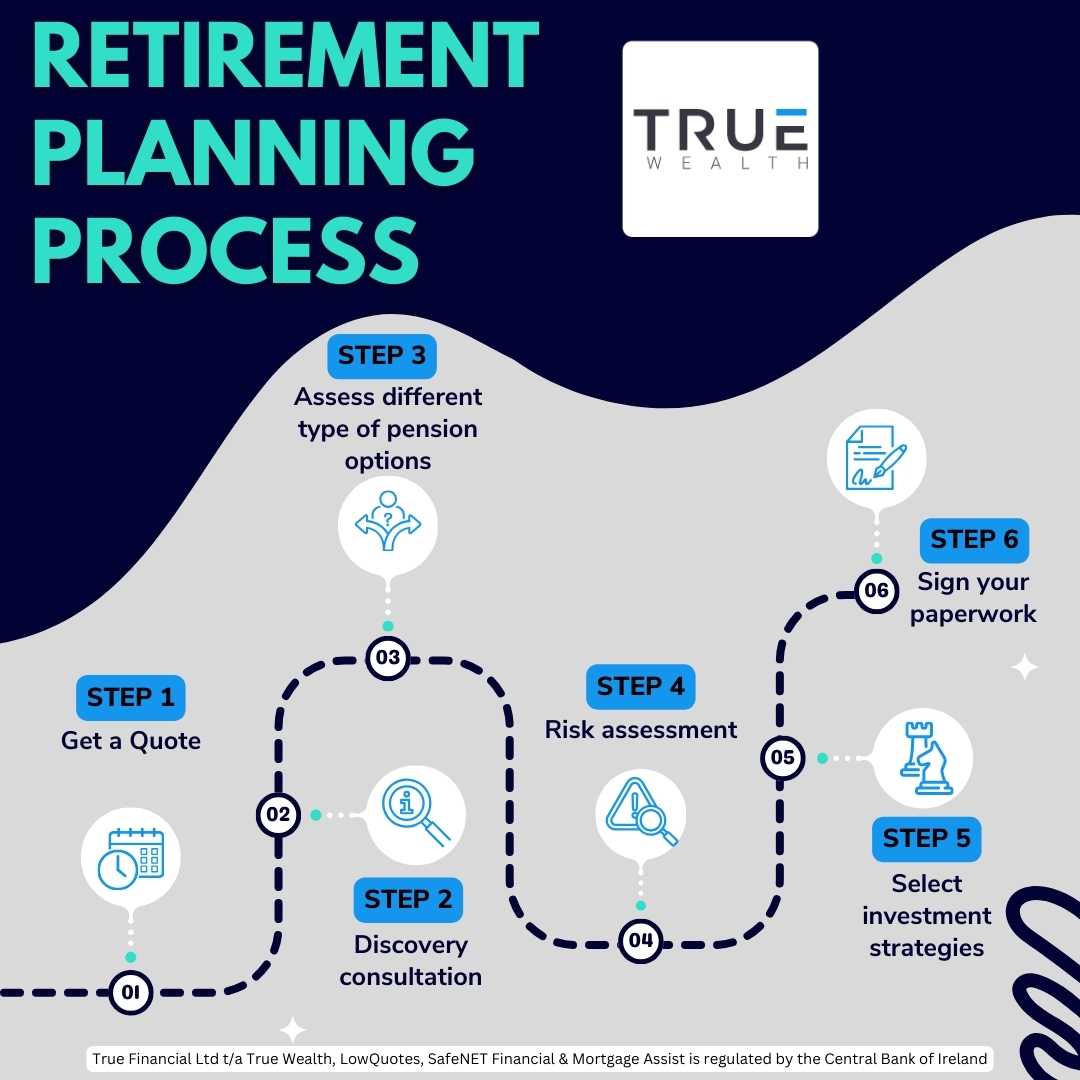

What is the Retirement Planning Process with True Wealth?

At True Wealth, we understand the importance of effective retirement planning and take pride in guiding our clients through each step of the process.

From the initial consultation to signing the paperwork, our dedicated team of financial advisors is with you every step of the way.

1. Get a quote

The first step in your Retirement Planning journey begins with getting a quote.

You will be asked some quick questions which will help us to pair you with a financial advisor to suit your unique situation.

2. Discovery consultation

During our discovery consultation, we provide you with a quote, and you’ll have the chance to have a one-on-one conversation with your dedicated financial advisor.

Your advisor will invest the time to grasp your unique situation and expectations, setting a solid groundwork for your retirement strategy.

Crafting a custom retirement plan involves a comprehensive fact-finding process.

This entails collecting data about your current financial position, your comfort level with risk, your preferred investment options, and the timeline for your retirement.

This step is pivotal in evaluating the appropriateness of various pension options.

3. Assess different types of pension options

Our team will present you with a range of pension options tailored to your specific needs.

We will explain the advantages and disadvantages of each, ensuring you have a clear understanding of your choices.

This comprehensive assessment helps you make an informed decision about your pension plan.

5. Risk Assessment

Understanding your risk tolerance is fundamental to the pension process.

We will work with you to assess your comfort level with different levels of risk.

This information will guide the development of an investment strategy that aligns with your preferences and goals.

6. Select investment strategies

Based on the risk assessment and your long-term objectives, we will recommend investment strategies that maximise your retirement savings.

Whether you prefer a conservative approach, an aggressive strategy, or something in between, our goal is to create a diversified investment portfolio that suits your needs.

7. Sign your paperwork

Once you are satisfied with your retirement plan and investment strategy, it’s time to sign the necessary paperwork to put your retirement plan in action.

Our team will walk you through all documentation, ensuring that you understand each aspect of your pension arrangement.

Embracing the Golden Years: A Guide to Post-Retirement Planning