9 Ways to Reduce Income Tax for the Self-Employed

Being self-employed in Ireland comes with its challenges and responsibilities, and managing your income tax is one of them.

However, with careful planning and a solid understanding of the tax system, you can implement strategies to legally minimise your tax liability.

In this blog post, we’ll explore some tips to help self-employed individuals in Ireland reduce their income tax burden.

Contribute to a Pension Scheme

One effective strategy to reduce income tax is by contributing to a pension scheme.

By actively participating in a pension plan, you not only secure your financial future but also benefit from immediate tax advantages.

Contributing to a personal pension can provide significant tax relief, as you can potentially enjoy up to a 40% reduction on your contributions.

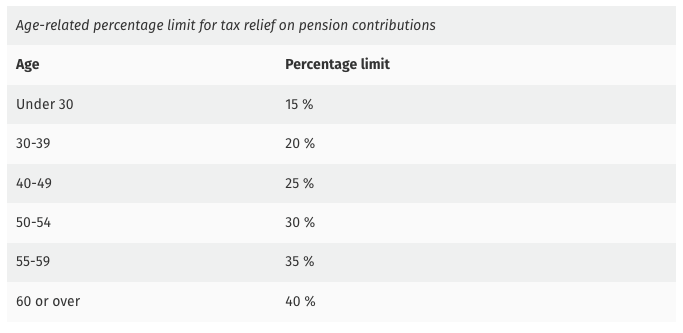

If you are self-employed, you can claim tax relief on pension contributions, subject to certain limits.

For instance, when you’re 29 years old, there’s a limit of 15% of your total income that can be allocated to your pension fund. This allocation limit incrementally increases as you progress through age groups, reaching its highest point at age 60 and beyond, currently standing at 40% of your salary.

Note that the maximum annual earnings considered for calculating tax relief is €115,000.

Explore our comprehensive retirement planning guide, which provides insights into the importance of having a private pension, how to plan your retirement at different stages of life, and a wealth of information on all aspects of pensions.

Boost your pension funds with AVCs

Additional Voluntary Contributions (AVCs) serve as an extra retirement savings avenue for individuals with established pension plans in Ireland, including occupational pension schemes or personal retirement savings accounts (PRSAs).

These voluntary contributions allow individuals to enhance their pension funds beyond the regular contributions made to their primary pension scheme, offering an additional means to strengthen their future retirement income.

This tax-saving approach is beneficial for higher earners, leading to reduced income tax obligations and enhancing overall financial planning and retirement savings.

Learn more about AVCs and their benefits by reading our article, How Additional Voluntary Contributions (AVCs) Can Supercharge Your Pension Savings.

Move company profits into your pension

A strategic approach to reducing income tax involves channelling company profits into your pension.

Traditional methods of profit extraction, such as dividends or personal asset acquisitions, expose business owners to higher tax burdens, ranging from 30% to 40%, as well as Capital Gains Tax, Capital Acquisitions Tax, and immediate tax liability for directors.

In contrast, transferring profits into your pension plan provides several advantages. These include no Benefit in Kind for the employer, immediate tax deductions, corporation tax relief, and exemptions from employer PRSI, Capital Gains Tax, and Corporation Tax.

Furthermore, pensions experience tax-free growth, and at retirement, a 25% tax-free lump sum is available, with the option to access the pension from the age of 50.

Alternatively, explore our article, “A Guide for Business Owners on Protecting, Extracting, and Growing Wealth in Ireland.“