Retirement Planning in Your 40s

How much should you save into your pension?

If you already have a pension, the right amount to save for it depends on your unique situation and disposable income.

Really and truly, you need help from a financial advisor that’s on your team, routing for you, and that’s us in a nutshell here at True Wealth. We are on team you!

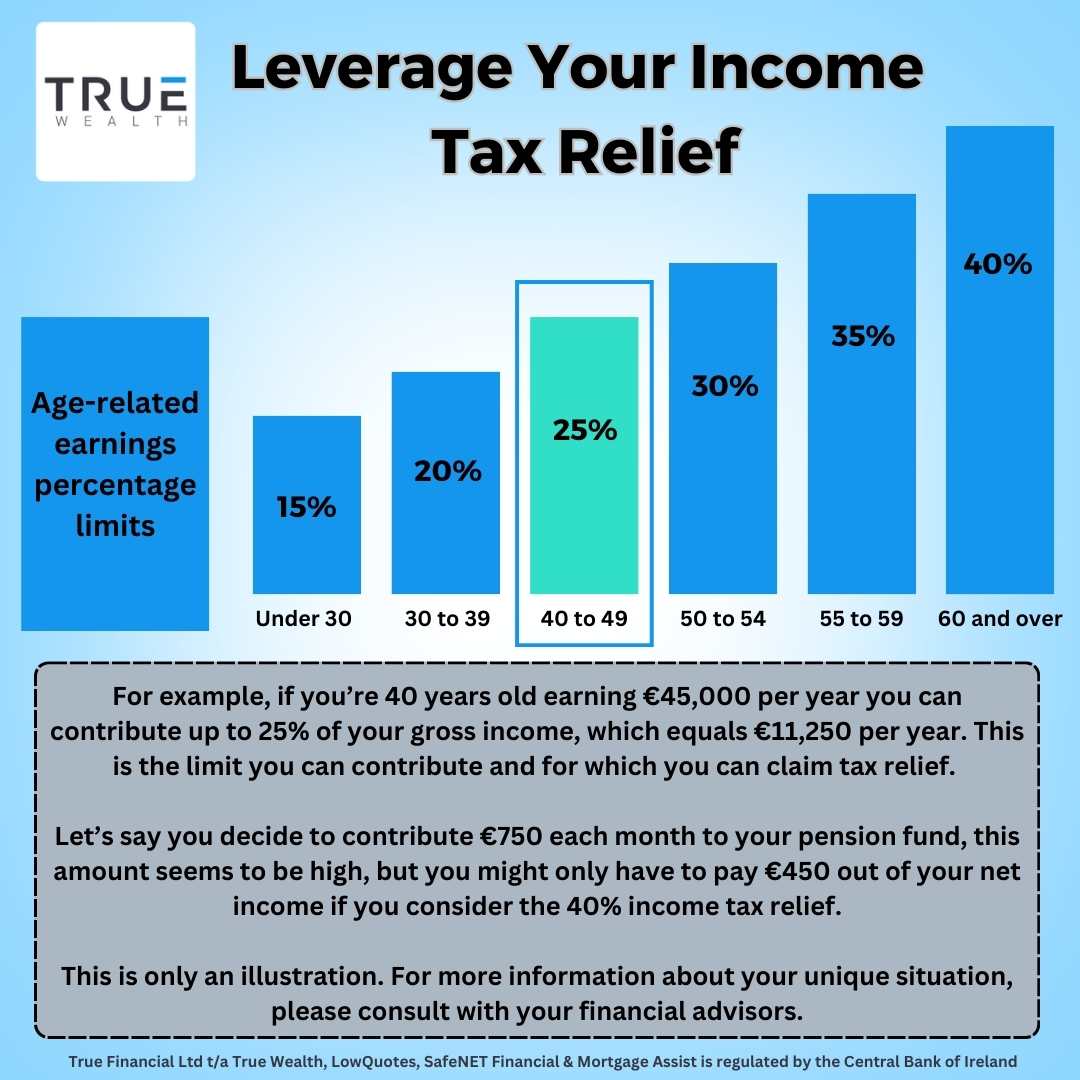

If you’re 40 years old, you can set aside up to 25% of your income for your pension claiming full tax relief. While this might seem like a lot, tax relief can make it easier to manage.

For instance, you’re earning €45,000 per year and decide to contribute €750 each month to your pension fund. This amount seems to be high, but you might only have to pay €450 out of your net income if you consider the 40% income tax relief.

4. Take Advantage of Tax Relief

Tax relief can be a powerful tool to boost your retirement savings. The Irish government encourages retirement savings by offering tax incentives to individuals who contribute to pension plans.

Contributions to these pension plans are often tax-deductible, meaning you can reduce your taxable income by the amount you invest. This results in immediate tax savings and more money available for your retirement fund.

By taking full advantage of available tax relief options, you not only reduce your current tax liability but also supercharge your retirement savings. This strategy makes your money work better for your future, bringing you closer to your retirement goals.

The exact tax benefits and rules can vary, so it’s advisable to consult with one of our financial advisors at True Wealth.

5. Increase Contributions Annually

Make a commitment to increase your retirement contributions each year, even if it’s a small increase. This practise can take advantage of compounding and help grow your retirement savings substantially over time, if your income increases or your expenditure reduces, offset it into your pension and earn the tax relief, it takes discipline, but it’s the good life.

Situations where you can increase contributions:

Promotion or pay rise

Both a promotion and a pay raise provide opportunities to increase your pension contributions. A promotion allows you to utilise the extra income while maintaining your lifestyle, while a pay raise, whether annual or as a bonus, can be allocated towards your pension contributions, accelerating your retirement savings.

Windfalls

Unexpected financial windfalls, such as an inheritance or a financial gift, might significantly increase your retirement savings. Consider increasing your pension payments with some of these windfalls rather than spending them all on expensive goods.

Reduction in Expenses

If you find ways to reduce your living expenses, consider redirecting the money saved into your retirement fund.

For example:

Consider that you’ve recently switched your mortgage to secure a lower interest rate, which has led to a substantial reduction in your monthly mortgage payments.

Additionally, you’ve reviewed your mortgage protection plan and found a more cost-effective policy that still provides the necessary coverage. These two financial decisions result in significant savings each month.

Before these changes, your mortgage and mortgage protection expenses were substantial portions of your monthly budget. However, with the new, more affordable terms, you now find yourself with extra funds at your disposal.

Instead of allowing this money to be absorbed by daily expenses or discretionary spending, you decide to be proactive in securing your retirement.

By redirecting these funds, you not only make the most of your reduced expenses, but also leverage the power of compound interest, ensuring that you’re well-prepared for your retirement in Ireland.

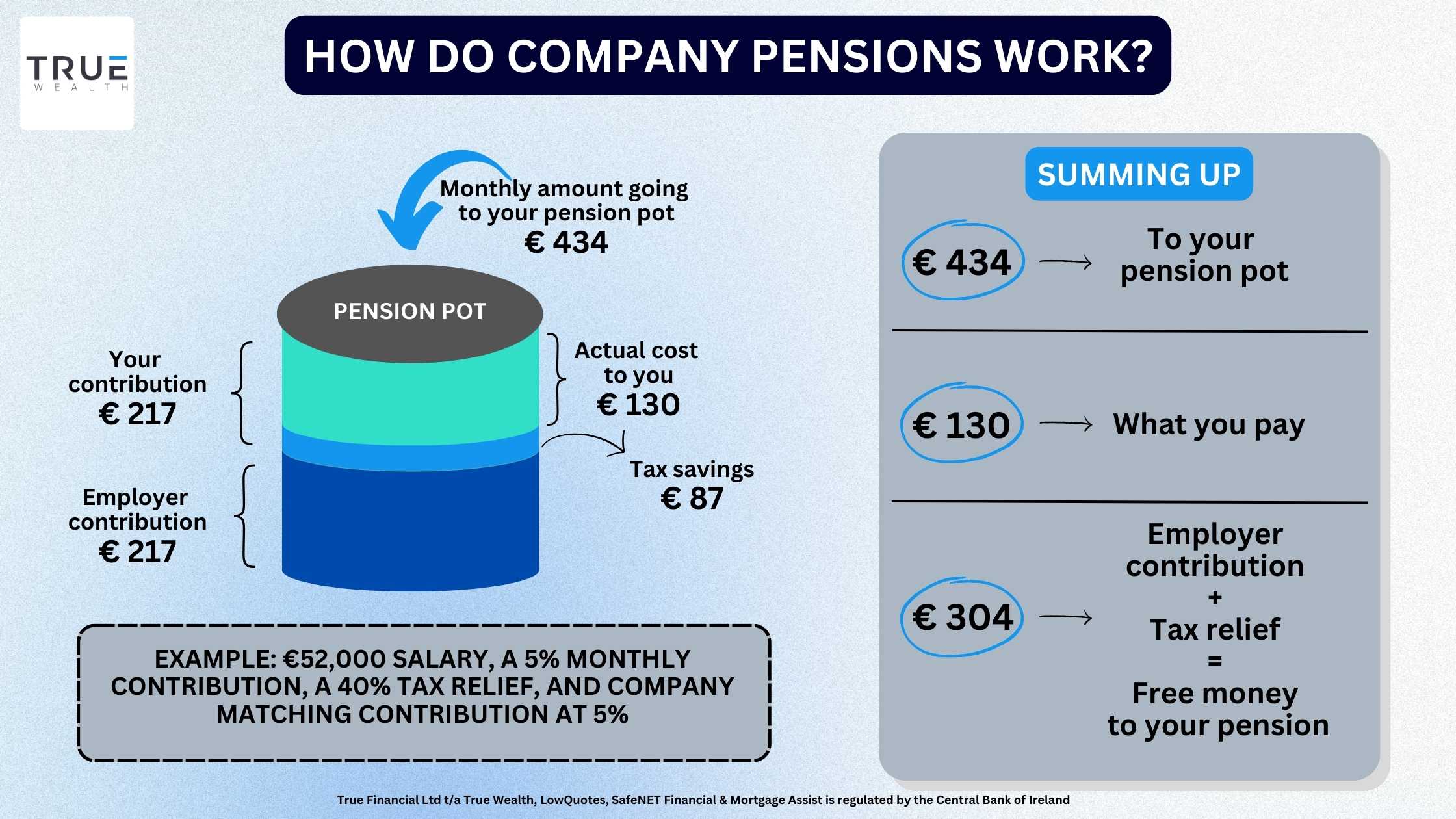

Employer Contributions Matching

If your employer offers a matching programme for your pension contributions, consider increasing your contributions to maximise this matching benefit. It’s essentially “free money” that can significantly boost your retirement savings.

Example:

Consider the scenario where you work for a company that offers a pension plan with an employer matching programme. This means that for every euro you contribute to your pension, your employer matches that contribution up to a certain percentage of your salary.

Initially, you’ve been contributing 5% of your monthly salary to your pension, and your employer matches that 5%. However, you’ve recently learned that your employer is willing to match contributions up to 8% of your salary.

Realising the potential benefit, you decide to increase your contributions from 5% to 8%. This change does not significantly impact your current net income since it’s a pre-tax contribution.

In essence, you’re taking advantage of this “free money” offered by your employer, and you’re essentially receiving a 3% salary increase in the form of matching contributions.

Over time, these additional contributions and the matching funds accumulate and grow through investments.

6. Optimise Your Asset Allocation

Asset allocation is a critical factor in your retirement strategy.

As you move through your 40s, consider revisiting your investment portfolio and making sure it aligns with your risk tolerance and retirement goals.

You might want to shift to a more conservative asset allocation to protect your savings from market volatility while still seeking opportunities for growth.

Regularly review your portfolio to maintain your desired asset mix. You can get professional guidance from our financial advisors at True Wealth.

7. Seek Professional Advice

Working with our financial advisors at True Wealth can provide you with tailored guidance, ensuring that your retirement savings plan aligns with your unique financial situation and retirement goals.

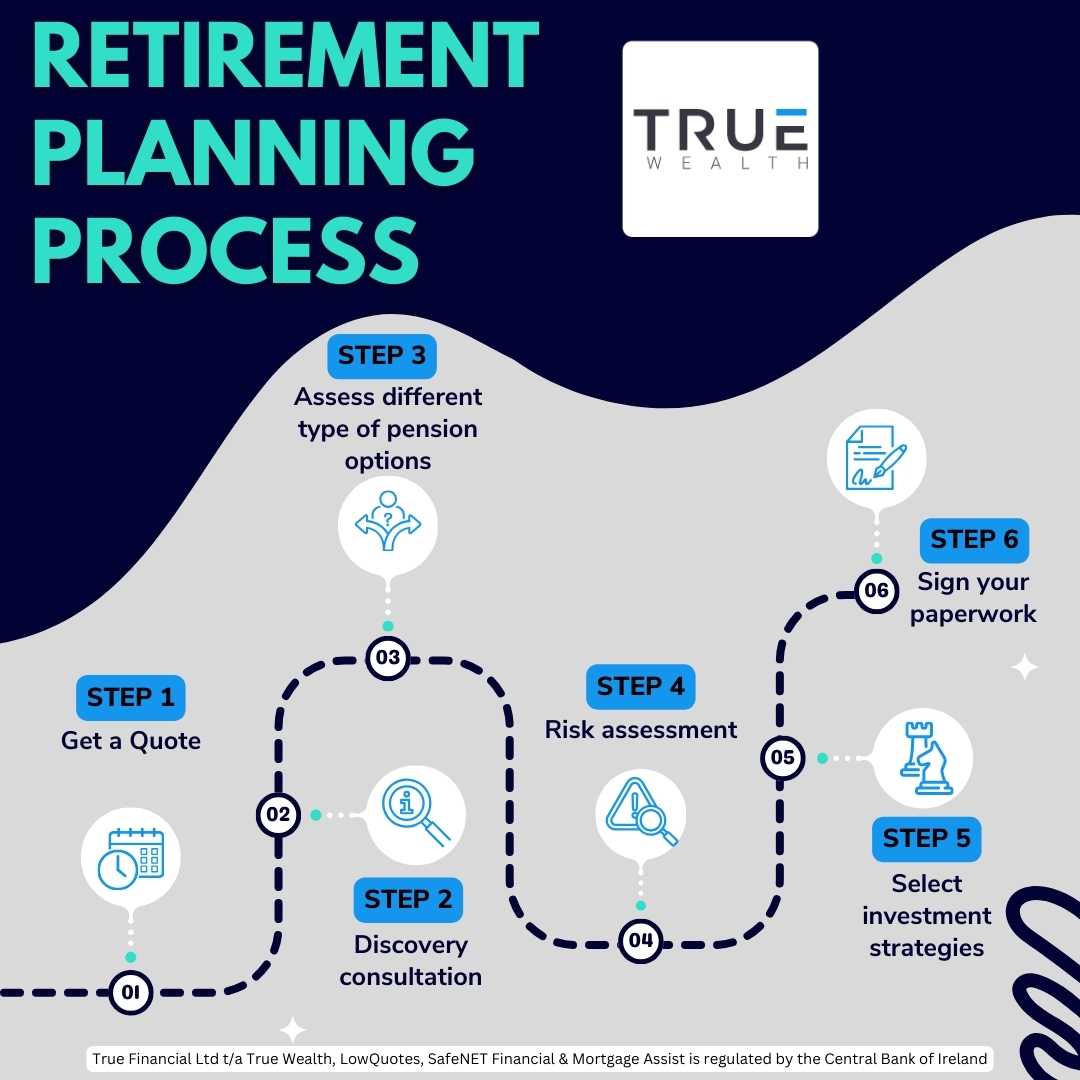

What is the Retirement Planning Process with True Wealth?

At True Wealth, we understand the importance of effective retirement planning and take pride in guiding our clients through each step of the process.

From the initial consultation to signing the paperwork, our dedicated team of financial advisors is with you every step of the way.

1. Get a quote

The first step in your Retirement Planning journey begins with getting a quote.

You will be asked some quick questions which will help us to pair you with a financial advisor to suit your unique situation.

2. Discovery consultation

During our discovery consultation, we provide you with your quote, and you’ll have the chance to have a one-on-one conversation with your dedicated financial advisor.

Your advisor will invest the time to grasp your unique situation and expectations, setting a solid groundwork for your retirement strategy.

Crafting a custom retirement plan involves a comprehensive fact-finding process. This entails collecting data about your current financial position, your comfort level with risk, your preferred investment options, and the timeline for your retirement.

This step is pivotal in evaluating the appropriateness of various pension options.

3. Assess different types of pension options

Our team will present you with a range of pension options tailored to your specific needs.

We will explain the advantages and disadvantages of each, ensuring you have a clear understanding of your choices.

This comprehensive assessment helps you make an informed decision about your pension plan.

5. Risk Assessment

Understanding your risk tolerance is fundamental to the pension process.

We will work with you to assess your comfort level with different levels of risk.

This information will guide the development of an investment strategy that aligns with your preferences and goals.

6. Select investment strategies

Based on the risk assessment and your long-term objectives, we will recommend investment strategies that maximise your retirement savings.

Whether you prefer a conservative approach, an aggressive strategy, or something in between, our goal is to create a diversified investment portfolio that suits your needs.

7. Sign your paperwork

Once you are satisfied with your retirement plan and investment strategy, it’s time to sign the necessary paperwork to put your retirement plan in action.

Our team will walk you through all documentation, ensuring that you understand each aspect of your pension arrangement.

Your Retirement in Your 40s with True Wealth

True Wealth understands that retirement planning cannot be standardised for everyone.

We work closely with you to develop a personalised strategy that aligns with your unique financial situation, lifestyle, and retirement goals. This tailored approach ensures that your plan is precisely designed to meet your expectations.

Seeking professional advice from True Wealth is an investment in your future. With our knowledge, you can navigate the complexities of retirement planning in Ireland and secure a comfortable retirement.

Don’t limit your retirement to the State Pension; partner with True Wealth for a well-structured and tailored retirement plan.

We are also experts in personal and business protection, savings and investments, pension tracing, personal and business financial planning, mortgages, and wealth extraction.