Retirement Planning in Your 50s and 60s

Steps to planning for your retirement in your 50s

1. Reevaluate your retirement goals

The first step to boosting your retirement savings later in life is to revisit your retirement goals.

Consider what you want your retirement to look like and adjust your financial plan accordingly.

Determine how much income you’ll need to maintain your desired lifestyle and create a new savings target.

2. Maximise Pension Contributions

In your 50s, it’s an excellent moment to begin reviewing your pension contributions and make sure that you’re on the right path to a financially secure retirement.

At this stage, your retirement is approaching, so you have a shorter time frame to save and invest for your retirement compared to someone in their 20s, 30s or 40s.

Make extra contributions

You have the flexibility to increase your pension contributions, whether you have a personal pension, an occupational pension, or a PRSA (Personal Retirement Savings Account).

Consider making Additional Voluntary Contributions (AVC) to your pension fund.

AVCs work as a top-up pension scheme. You can choose to make AVCs through regular contributions or as lump-sum payments, based on your personal preference and the guidelines of your pension plan.

Usually, contributions to AVCs are deducted from your pre-tax income, offering potential tax benefits.

3. Review Your Investment Portfolio

As you approach retirement, consider shifting your investments towards more conservative options to protect your savings from market volatility.

Consult a financial advisor at True Wealth to review your investment portfolio.

4. Take Advantage of Tax Benefits

One of the main advantages of making contributions to a pension in Ireland is the tax relief available. When you contribute to a pension scheme, you become eligible for tax relief based on your marginal tax rate, provided you stay within the annual limits.

This implies that if you are a higher-rate taxpayer paying 40% income tax, you have the opportunity to claim an equivalent amount in tax through your pension contributions.

For instance, if you decide to contribute €1,000 to your pension and are subject to a 40% income tax rate, your actual cost after tax deductions will be only €600.

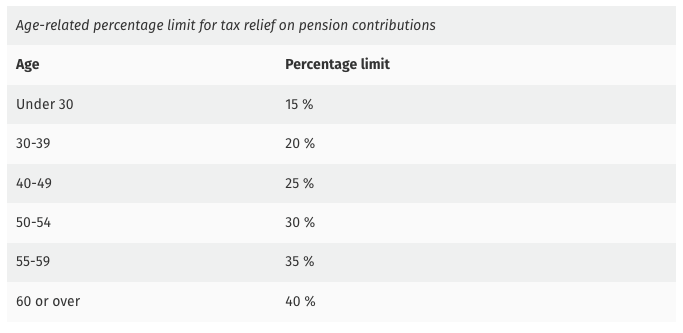

Pension Contribution Limits

In Ireland, annual pension contributions eligible for tax relief are subject to age and income-based limits, ensuring full relief within those boundaries. Earnings up to €115,000 annually are considered for tax relief calculations.

These limits might not apply to directors, key employees, or professional sports people.