6 Compelling Reasons Business Owners Need Holistic Financial Planning

6 Compelling Reasons Business Owners Need Holistic Financial Planning

Financial planning is a cornerstone of business success. Yet, many business owners tend to focus on the day-to-day operations of their companies while neglecting their long-term financial strategies.

This is where holistic financial planning for business owners comes into play. In this blog post, we’ll explore six compelling reasons business owners need holistic financial planning to ensure the prosperity and sustainability of your company.

Comprehensive Financial Strategy

Holistic financial planning provides business owners with a comprehensive strategy for your financial future.

It takes into account not only the current financial strategy of the business but also personal financial goals, potential risks, and long-term aspirations.

This ensures that every aspect of your financial life is covered, helping you make informed decisions at every stage of your business journey.

1. Risk Management

Running a business involves inherent uncertainties and challenges, making effective risk management an indispensable aspect of its success.

Whether it’s financial volatility, operational disruptions, legal compliance, unexpected leadership transitions, or the unforeseen death of a key person.

Identifying, assessing, and mitigating these risks is crucial for safeguarding the business’s long-term stability.

With a well-structured plan in place, you can actively address potential challenges and navigate turbulent times more effectively, safeguarding your business.

Example of The Impact of Losing a Key Person

One of the inherent risks that businesses face is the potential loss of a key person due to death or serious illness.

When such a critical individual is no longer available, it can have profound repercussions for the business, including significant financial losses, challenges in meeting bank loan obligations, and difficulties in paying off outstanding debts.

Consider a scenario where a thriving company heavily relies on its CEO, Fiadh, to drive growth and maintain crucial relationships with clients and partners.

In this case, Fiadh’s unexpected passing or severe illness would disrupt the business in several ways, such as:

Financial Losses: The business may experience an immediate drop in revenue and profitability, as clients and partners may lose confidence in the company’s ability to deliver without Fiadh’s leadership.

Debt Payment Challenges: Meeting existing debt payments, including loans and other financial obligations, could become more challenging due to reduced cash flow and financial uncertainty.

Director’s Shares: The unexpected loss of a key person can pose a complex challenge to smoothly transitioning ownership, particularly when it comes to director’s shares.

See insurance planning below.

2. Tax Strategies

Taxation can be a significant expense for businesses. Holistic financial planning includes strategies for optimising your tax situation.

By working closely with True Wealth, you can identify legitimate tax-saving opportunities that can help reduce your tax liability and increase your after-tax income.

Listen to our Pension Specialist, Carl Cassidy explain a clever way to save thousands on tax if you are a company owner.

Business Owner Financial Plan Quote

3. Retirement Planning

As a business owner, planning for retirement is essential, but it’s often overlooked. The idea of retiring or stepping down from your leadership role might not always be top of mind.

However, it’s crucial to emphasise the importance of maximising your contributions to build a substantial wealth portfolio that will enable a comfortable retirement in a tax-efficient manner.

Holistic financial planning ensures that your retirement needs are integrated into your financial strategy.

We can assist you in realising your retirement ambitions, set savings goals, and create an investment plan that aligns with your retirement goals. It’s essential to recognise and take full advantage of the valuable tax benefits at your disposal.

Executive Pension for Employees or Employers

Utilising an executive pension plan, also known as a company pension scheme, serves as an investment vehicle tailored for directors and employees to build retirement savings.

An executive pension plan is designed to facilitate retirement savings for employees, company owners and directors.

This plan extends the opportunity for both employees and employers to benefit from tax relief on their contributions.

PRSAs

Personal Retirement Savings Accounts (PRSAs) offer an attractive retirement planning option for business owners.

These individual pension plans provide flexibility and convenience for entrepreneurs and self-employed individuals looking to secure their financial future.

PRSAs enable business owners to save for retirement while enjoying valuable tax benefits.

With the ability to choose their contribution levels and investment options, PRSAs empower business owners to tailor their retirement strategy to their unique needs and circumstances.

Furthermore, PRSAs are portable, allowing for easy transfer if a business owner decides to change careers or take on a different role within their business.

In a world where retirement planning is paramount, PRSAs offer an accessible and practical solution for business owners seeking to build a secure financial foundation for their later years.

Get in touch with True Wealth; we provide expert guidance throughout the pension journey for business owners.

Business Owner Financial Plan Quote

4. Investment Planning

Managing personal and business investments can be complex. Holistic financial planning includes diversification strategies that minimise risks and maximise returns.

We can help you build a diversified investment portfolio that aligns with your financial goals, ensuring that your assets are protected and grow steadily over time.

Small Business Owners

For small business owners, the temptation to invest primarily in their own ventures can be overwhelming.

However, there may be opportunities to save in various aspects of your finances, freeing up capital to diversify your investment portfolio.

Diversifying your investments is a fundamental aspect of risk management.

Medium to large business owners

If you are a medium to large business owner and have yet to diversify your investments beyond your business, we strongly recommend reaching out to us. It’s important to align a tailored investment strategy with both your personal and business objectives.

If you currently have investments

For those who currently have investments in place, it’s essential to conduct periodic reviews as your business grows.

Your risk profile naturally evolves as you age, and your financial goals change accordingly.

Generally speaking, your attitude towards risk should get lower the older you get.

During a review, it’s important to assess various factors, including your existing management fees, allocation rates, and portfolio diversification.

These assessments should include shifts in economic landscapes, ethical responsibilities, and sustainability considerations.

To guarantee that your investments smoothly correspond with your business and personal financial objectives, you can choose between structured monthly savings plans and lump-sum investments based on your financial preferences and goals.

Which option best describes your situation?

I have received a sum of money and want to invest it.

I want to invest money monthly into a savings plan

5. Insurance Planning

Tax relief is available on the insurances below

Incorporating insurance planning is a fundamental component of comprehensive financial planning for business owners seeking to shield your business or investment property from the financial repercussions of a severe illness or death.

KeyPerson Life Insurance

Key Person Insurance is essential for businesses, offering protection against the potential loss of a key individual whose contributions significantly impact the company’s success.

In the unfortunate event of the key person’s death or serious illness, the policy provides a lump sum to offset financial losses and can be used to address issues like bank loans or debts for which the key employee may have provided a personal guarantee.

This type of life insurance is suitable for businesses of all sizes that rely on a highly valuable employee with substantial financial or strategic importance to the company.

Co-director Insurance

Co-director Insurance is a valuable safeguard for businesses, ensuring stability in the face of unexpected events such as a director’s death or illness.

This insurance allows the company to purchase the deceased director’s shares from their next of kin, granting the remaining directors full control of the company.

It also offers peace of mind for the family of the deceased, who may not wish to take on the director’s role.

In the event of the director’s passing, the policy provides a lump sum, which can be used to acquire the shares, ensuring business continuity and financial security.

Corporate Co-director Insurance

Corporate Co-Director insurance is crucial for companies whose directors play vital roles as major shareholders and decision-makers.

The policy offers security in the unfortunate event of a director’s serious illness or death, ensuring that funds are available for the repurchase of shares, thus mitigating potential difficulties for surviving directors and the deceased’s successors.

To establish this business protection, it’s essential to address both legislative and taxation considerations with the guidance of legal and taxation advisors.

Premiums, paid regularly throughout the policy term, are determined by factors such as the director’s share value and the company’s turnover.

In the event of a director’s passing, the policy provides a lump sum, facilitating the purchase of shares from next-of-kin.

Partnership Insurance

Partnership Insurance is vital for business partnerships built on years of collaboration, friendship, and mutual support.

The death of a partner can be emotionally distressing and financially destabilising, potentially requiring the remaining partners to compensate the deceased’s estate for their stake in the partnership.

This insurance offers the necessary funds to ensure a smooth transition, allowing the partnership to continue without involving next-of-kin.

Legal and taxation advisors should be consulted before obtaining a policy, and premiums are influenced by factors like the partnership’s value.

In the unfortunate event of a partner’s death, the policy provides a lump sum for compensation, making Partnership Insurance a valuable choice for partners in any business arrangement.

Business Owner Financial Plan Quote

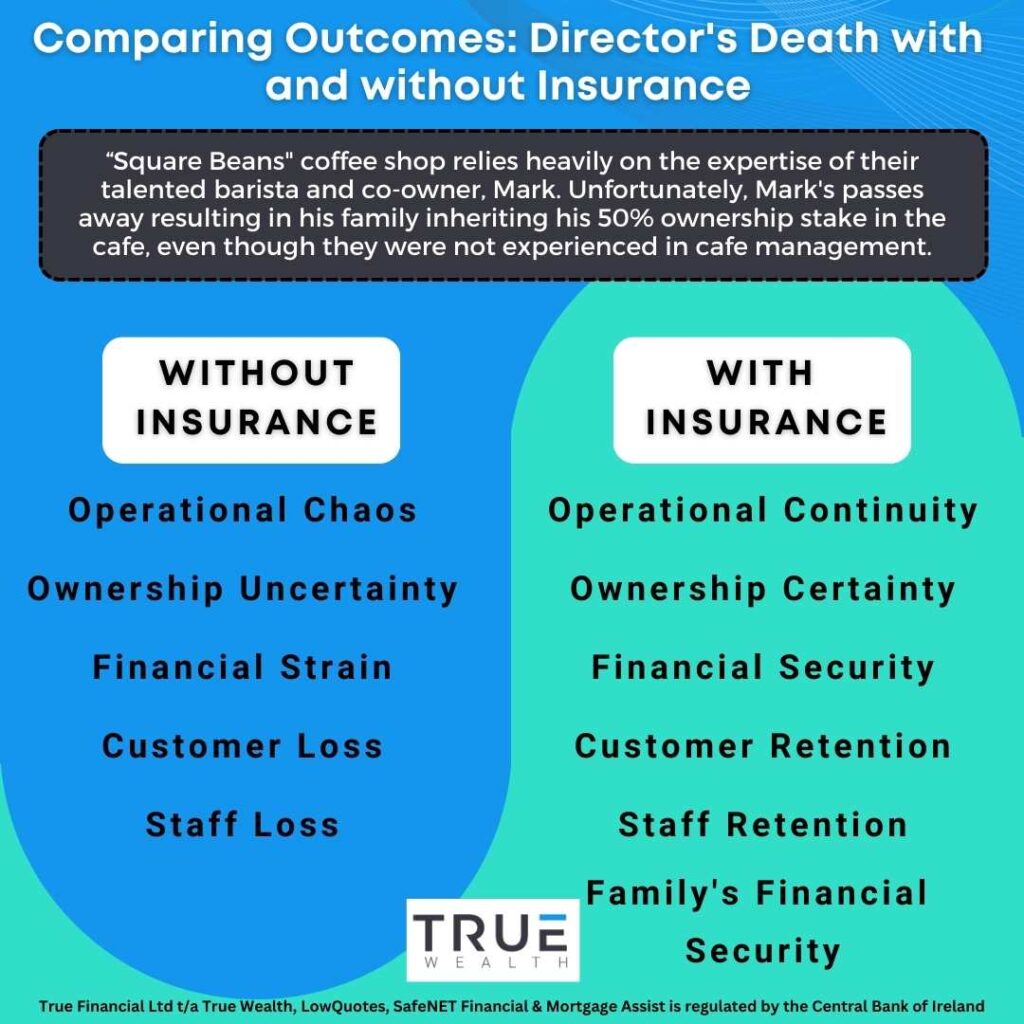

Example: Director's death with insurance vs. without insurance

The sudden and tragic loss of Mark, the skilled barista and co-owner of “Square Beans” coffee shop, had profound consequences for the business. Without the protection of Key Person Insurance, the establishment faced several significant challenges:

Outcome Without Key Person Insurance:

- Operational Chaos: Mark’s absence leaves a gap in making coffee, causing confusion and longer waiting times for customers.

- Ownership Uncertainty: Mark’s family now owns half of the coffee shop, but they don’t have the skills to contribute to its daily operations.

- Financial Strain: The business faced financial strain as it struggled with the loss of revenue resulting from a decline in customer satisfaction and a decrease in staff retention.

- Customer Loss: Some regular customers leave due to the decline in service quality.

- Staff Loss: Worried about the cafe’s future, other staff members start seeking new jobs.

Outcome With Key Person Insurance:

- Operational Continuity: With Key Person Insurance in place, the business would have had access to financial resources to hire and train temporary staff or bring in additional support, ensuring minimal disruption to daily operations.

- Ownership Certainty: The insurance policy could have facilitated a smooth transition of Mark’s ownership stake, ensuring that the business remains in capable hands or facilitating a buyout arrangement that preserves business continuity.

- Financial Security: The financial support from the insurance policy would have alleviated the strain on the coffee shop’s finances, allowing it to weather the immediate impact of Mark’s loss.

- Customer Retention: The ability to maintain product quality and service standards would have helped retain loyal customers and prevent a decline in sales.

- Staff Retention: With measures in place to ensure operational stability and financial security, staff members would have been more likely to remain with the business during a challenging period.

- Family’s Financial Security: Mark’s family would have received a payout from the Key Person Insurance, providing them with financial security and support during a difficult time.

In this straightforward illustration, Key Person Insurance proves essential in maintaining the coffee shop’s stability, ensuring it can keep serving its loyal customers, and providing financial security for both the business owners and Mark’s family.

Pension Term Assurance

Pension Term Assurance is a life insurance policy designed to provide a lump sum payout in the event of the policyholder’s death during the term.

This unique policy structure leverages available tax relief under pension legislation, and you don’t need an existing pension plan to take advantage of it.

Eligibility includes being self-employed or working in non-pensionable employment.

Notably, one of the main benefits is the ability to claim full tax relief at your marginal tax rate on premiums, potentially making this valuable protection up to 40% more cost-effective than a standard Term Assurance policy.

Executive Income Protection

Executive Income Protection policy is another valuable insurance option for business owners.

This not only provides a contingency for your company in times of need but also guarantees the continuity of your pension contributions in the event of unforeseen circumstances.

With Executive Income Protection, you can safeguard the funds allocated to your company pension while ensuring that, in case of illness or injury that prevents you and/or your employees from working.

Such policies will yield up to 75% of your salary, inclusive of state benefit (if applicable). Additionally, it’s worth noting that the company covers the premiums, which can be categorised as a business expense.

Get in touch with True Wealth; we are equipped to offer expert guidance throughout the insurance journey for business owners.

6. Cashflow Planning

A pivotal component of a Business Owner Financial Plan involves the utilisation of our Online Cashflow Model, a tool designed to assess your existing cash flow and generate potential scenarios.

This empowers you to visualise the potential trajectory of your financial future under various circumstances.

Additionally, we enhance the robustness of our proposed solutions by stress-testing them, employing deterministic modelling techniques up to 10,000 times.

This approach is rooted in the understanding that markets exhibit non-linear behaviour, and thus, future cash flow models should mirror this reality.

The stress test, known as ‘Monte Carlo,’ takes into account your current risk tolerance, market trends, and provides you with pessimistic, optimistic, and average outcome scenarios, offering a comprehensive view of potential financial pathways.

Get Started Today with True Wealth

We will assist you in gaining a holistic perspective and taking meaningful action, ultimately leading to improved outcomes for both your family and your business.

In addition, we offer a valuable second opinion on critical financial decisions, ensuring that you make well-informed choices that align with your goals and aspirations.

We at True Wealth are experts in personal and business financial planning, retirement and pension planning, pension tracing, savings and investments, protection, mortgages, and wealth management.

At True Wealth, our financial planning services are designed with business owners in mind, recognising that each individual’s circumstances, goals, and risk tolerance are unique.

Contact us today; we are here to assist you in crafting a personalised financial plan that caters to your distinct needs and aspirations.

Business Owner Financial Plan Quote

All our content has been written or overseen by a qualified financial advisor. However, you should always seek individual financial advice for your unique circumstances.