What’s the difference between auto-enrolment and private pension schemes?

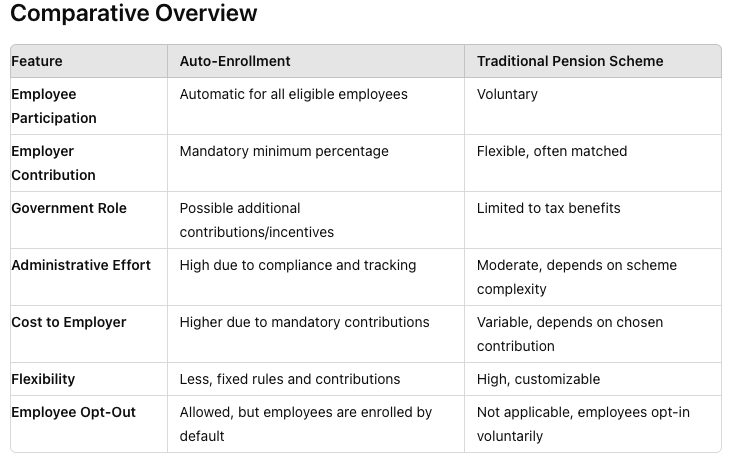

Auto-enrolment automatically enrols all eligible employees in a pension scheme, requiring both employers and employees to contribute a set minimum percentage of the employee’s salary.

Employees can opt out if they choose, but they are enrolled by default. The government may also offer additional contributions or incentives to boost employee savings.

Private pension schemes are voluntary, with employees choosing to join and contribute. Contributions are flexible and may be matched by employers. These schemes can be tailored to fit the business’s and its employees’ needs.

As a business owner, understanding these differences will help you decide which pension scheme aligns best with your business goals and employee needs.

How Does Tax Relief Differ Between Auto-Enrolment and Private Pensions?

When it comes to retirement savings, understanding the differences in tax relief between auto-enrolment and private pensions is crucial. Both systems offer tax advantages, but the specifics can vary significantly.

Auto-Enrolment Pension Tax Relief

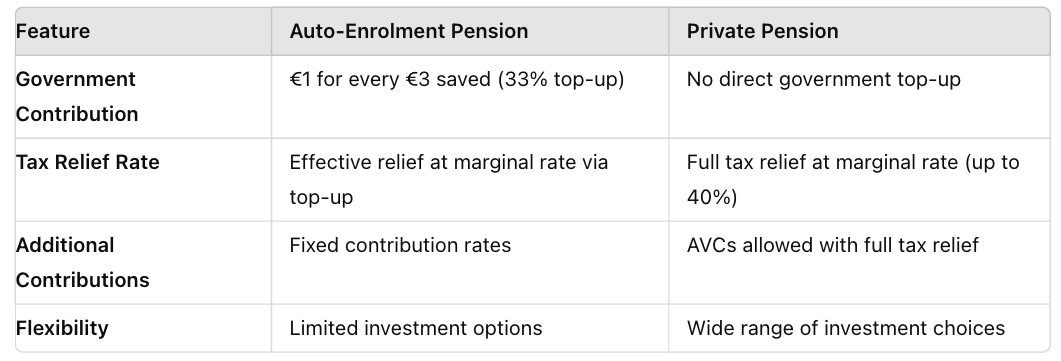

Government Top-Up: In the auto-enrolment scheme, the Irish government contributes €1 for every €3 saved by the employee. This translates to a 33% state top-up on contributions.

Employee Contributions: Contributions are made from gross salary before tax is applied, which means employees effectively get tax relief at their marginal rate. However, the direct government top-up is a fixed rate.

Private Pension Tax Relief

Marginal Tax Rate Relief: Contributions to private pensions, such as Personal Retirement Savings Accounts (PRSAs) or occupational pension schemes, qualify for tax relief at the individual’s highest marginal tax rate. This means if you pay tax at 40%, you get 40% tax relief on your contributions.

Additional Voluntary Contributions (AVCs): Private pensions allow for AVCs, which can also benefit from tax relief at the individual’s marginal rate. This offers more flexibility for higher earners to maximise their tax benefits.

More Flexibility: Private pensions often offer more flexibility regarding investment choices and contribution levels, potentially allowing for higher returns or tailored retirement strategies.

Summary of Tax Relief Comparison

Both auto-enrolment and private pensions offer significant tax advantages, but they cater to different needs and income levels. Auto-enrolment provides a straightforward, accessible way to save for retirement with a 33% government top-up, making it particularly beneficial for lower to middle-income earners.

On the other hand, private pensions offer more flexibility and higher potential tax relief at the marginal rate, which can be more advantageous for higher earners who want to maximise their retirement savings.

Why Private Pension Scheme Might Be a Better Option for Your Company and Employees Than Auto Enrolment

While auto-enrolment provides a basic level of retirement savings, it often comes with generic investment options and contribution rates that may not suit all employees.

On the other hand, an occupational pension scheme, for example, allows the company to negotiate better terms, offer higher employer contributions, and select investment options that align with the company’s values and the financial goals of its employees.

This personalised approach can enhance employee satisfaction and retention, ensuring that the pension plan is a valuable and appreciated benefit rather than a mere compliance measure.

Customisation and Flexibility

Private Pensions: Allow customisation over auto-enrolment schemes, letting companies tailor private pension plans to meet employees’ specific needs, including investment options that match their risk tolerance and retirement goals.

Auto Enrolment: Typically follows a one-size-fits-all approach. Investment choices and contribution levels are often standardised, which provides less flexibility for individual employees.

Improved Employee Engagement and Satisfaction

Private Pensions: Personalised pension plans make employees feel valued, boosting morale, loyalty, and job satisfaction. Tailored financial advice demonstrates a commitment to their long-term financial well-being.

Auto Enrolment: While it ensures that employees are saving for retirement, it might not engage them on a personal level. The lack of customisation can lead to lower employee engagement with their pension plan.

Competitive Advantage in Recruitment

Private Pensions: Providing a private pension can set your company apart in the competitive job market. High-quality candidates often look for comprehensive benefits packages, and a superior pension plan can be a deciding factor. This can be particularly advantageous for attracting senior or highly skilled professionals who will likely value enhanced retirement benefits.

Auto Enrolment: Since it is a standard offering across many businesses, it does not provide a significant differentiator when competing for top talent.

Tax Efficiency and Cost Management

Private Pensions: Can be structured in a tax-efficient manner, benefiting both the company and its employees. Employers may have more control over the contributions and timing, allowing for better cash flow management and potential tax advantages.

Auto Enrolment: While still offering tax benefits, the mandatory nature and predefined contribution rates may limit the financial flexibility for both employers and employees.

Benefits of Occupational Pension Scheme for Employers and Employees

Occupational pension schemes offer numerous benefits for both employers and employees, making them a vital component of a comprehensive employee benefits package.

For employers, providing an occupational pension scheme enhances their ability to attract and retain top talent. Additionally, contributions to these schemes can be tax-efficient, offering potential financial savings for businesses.

Employees, on the other hand, gain a structured and reliable means of saving for retirement. Occupational pension schemes often include employer contributions, which significantly boost the total savings compared to individual efforts alone. These schemes also provide tax advantages, as contributions are typically made before tax is deducted, increasing the overall value of the retirement savings.

Read our article here for more insights into the benefits of occupational pension schemes.