What Are the Benefits of Group Income Protection for Employers?

Attract and Retain Talent

Offering income protection is a competitive benefit that shows you care about your employees’ wellbeing, helping you stand out in a competitive job market.

Reduced Absence Costs

Early intervention and support services often reduce the length of absence, meaning employees return to work faster, saving your business time and money.

Boost Employee Productivity and Loyalty

Knowing they’re protected, employees are more likely to feel secure and focused, contributing positively to your company culture and performance.

Tax-Deductible Premiums

Premiums paid by the business are usually treated as a tax-deductible expense, offering potential cost-efficiency for your company.

Simple Administration for Groups

Group policies cover multiple employees under one plan. This makes it easier to manage than individual arrangements and can be more cost-effective.

Key Features of Group Income Protection

- Start Small: Available for as few as three employees, with a minimum annual premium of €1,000. This is ideal for SMEs.

- Customisable: Tailor benefits by employee group, from basic to enhanced protection.

- Long-Term Cover: Policies can run up to age 68, aligning with Ireland’s retirement age.

- Early Support Services: Some providers offer intervention and rehabilitation support within the first month of absence, increasing the chances of recovery and return to work.

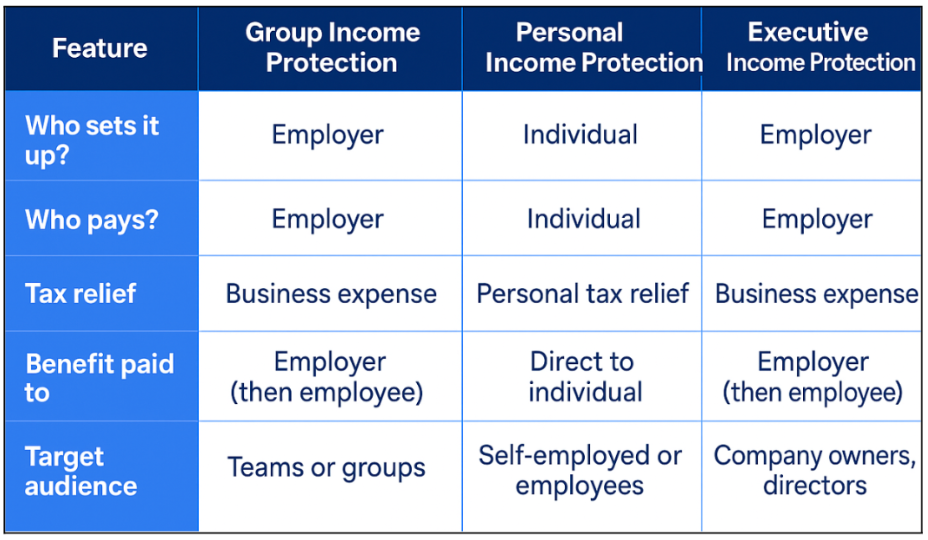

What’s the Difference Between Personal Income Protection and Executive Income Protection?

It’s important to understand how Group Income Protection fits alongside other types of income protection, such as Personal and Executive Income Protection, especially when deciding what’s best for different members of your team.

Personal Income Protection is ideal for self-employed individuals or employees seeking their own cover. They pay the premiums personally and can claim tax relief on them. If they can’t work due to illness or injury, the benefit is paid directly to them, helping to replace a portion of their income while they recover.

Executive Income Protection, on the other hand, is set up and paid for by a company on behalf of a specific employee, usually a director or key team member. The business pays the premiums (typically tax-deductible), and the benefit is paid to the company if the employee is unable to work due to illness or injury. The company then passes that benefit on to the employee through payroll. Executive policies can cover higher incomes, including salary and dividends, and often include more flexible or enhanced features tailored to senior roles.

Group Income Protection is different in that it allows you, as an employer, to provide income protection to multiple employees under one policy. It’s typically offered to all staff and is paid for by the business. The premiums are usually tax-deductible, and if an employee is unable to work long-term due to illness or injury, the benefit is paid to the employer and then passed on to the employee through payroll (taxed as income).