Retirement Planning in Your 20s

More Time to Contribute

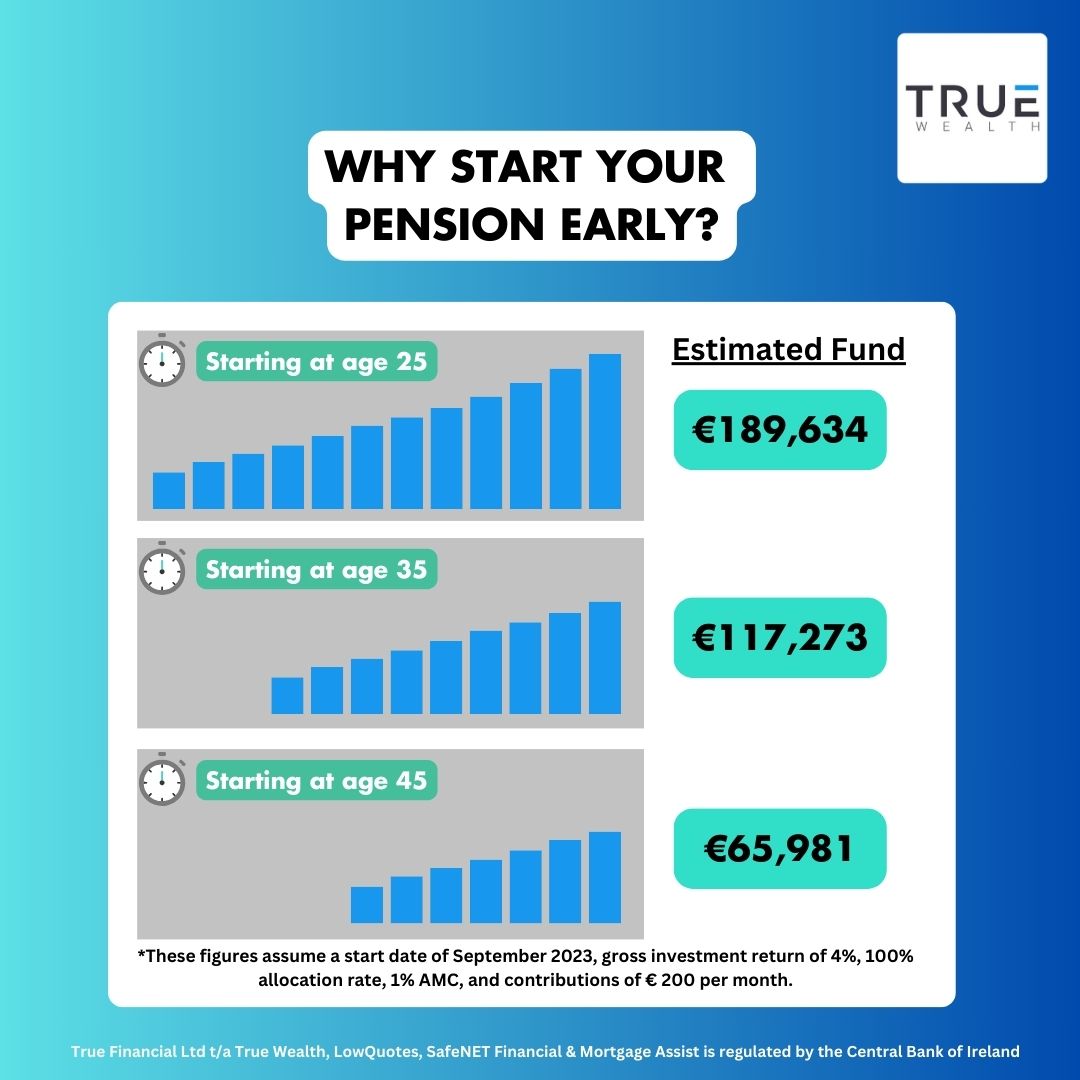

Beginning retirement planning at a young age provides you with the gift of time. The longer you save and invest, the more your money can grow through the magic of compounding. I’ll say it again: we love compound interest. (literally free money)

This means you’ll need to contribute less each month to reach your retirement goals, or you can just have a really nice and comfortable life in retirement, you know you deserve it.

State Pension May Fall Short

In 2023, the weekly state pension rate in Ireland is €265.30, and the retirement age is 66.

According to the Central Statistics Office the average weekly wage was €900.26 in Q4 2022.

We know and understand that you may not need your historic wage at retirement age. But the fall off is steep and it’s recognised to be a real issue in this country. Why else would the government give you back up to 40% of your payments? You know it’s a serious issue when the government incentivises you heavily to provide for your own retirement. (So you won’t be leaning on them in the future)

While the State Pension offers essential support, it might not be sufficient to maintain your desired lifestyle during retirement.

As your career progresses, your earnings will likely increase. When you retire, the gap between your salary and the State Pension becomes more evident. Early retirement planning helps bridge that gap.

Longer Life Expectancy

People in Ireland are living longer, with an average life expectancy of 93.6 years for those born in 2021. This is good news for all of us, but needs to be planned for.

This extended lifespan means that you may need more savings to maintain a comfortable standard of living in retirement.

Starting early allows you to accumulate the necessary funds for a longer retirement.

Compound Interest

Did I say we love this?… Time is your greatest ally when it comes to building wealth through investments.

By starting your pension early, your money has more time to grow through compounding.

This means that the interest you earn on your investments generates more interest over time, creating a snowball effect that can significantly boost your retirement savings.

Tax Benefits

Private pensions offer excellent tax incentives. Contributing to your pension can reduce your taxable income, providing an immediate financial benefit. So the money goes into my pension rather than to the government? Okaaaaay, I think I will pay myself instead of the government through higher income tax. It’s a no brainer folks.

Additionally, your pension fund grows tax-free until retirement, allowing you to maximise your savings.

Explore our article that delves into 9 Reasons to Have a Private Pension in Ireland. By reading our article, you’ll be able to understand how important having a private pension is and make informed decisions.

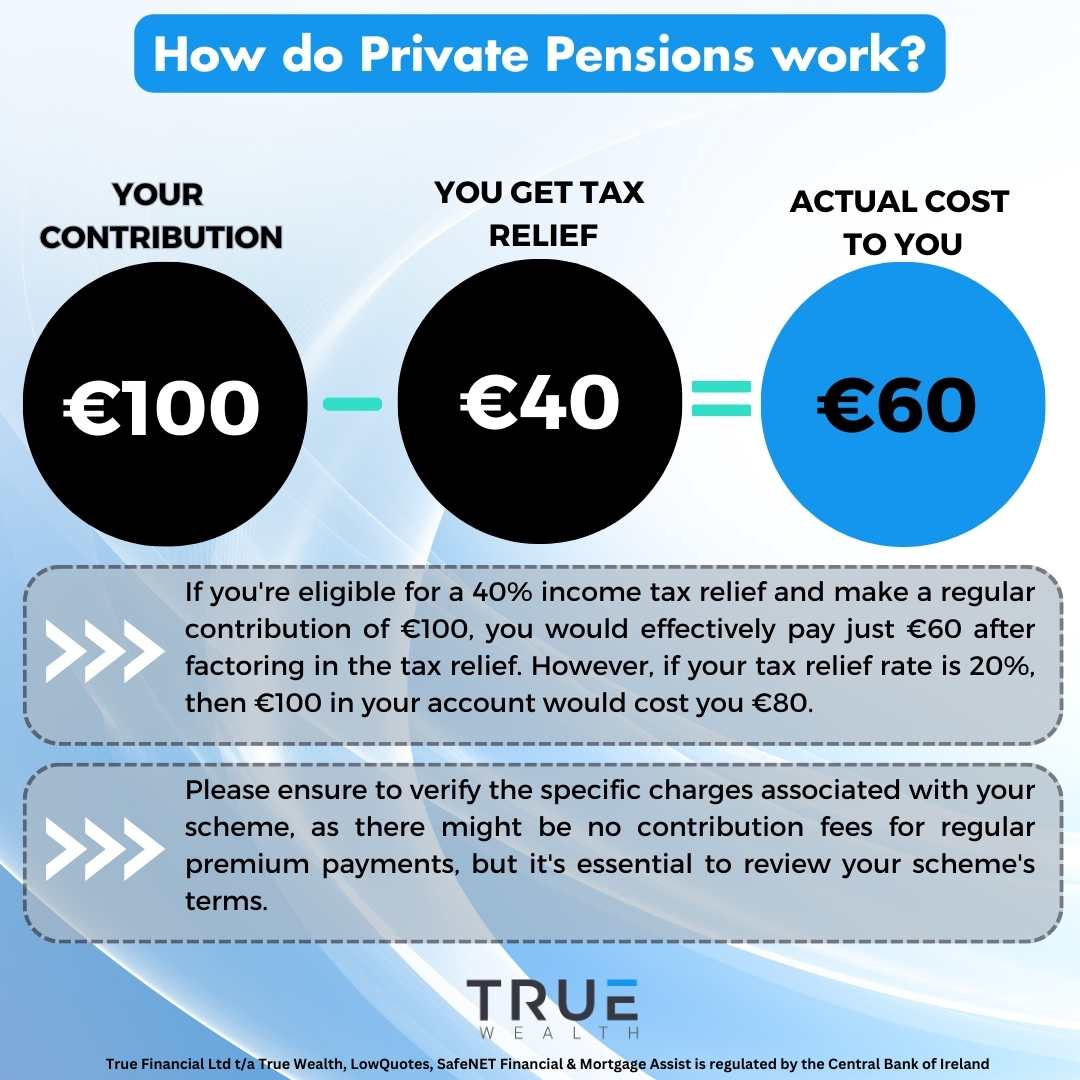

How do private pensions work?

When you put money into your private pension, the government offers tax relief on those contributions.

This means that the money you contribute to your pension is deducted from your taxable income, reducing the amount of income that is subject to taxation.

As a result, you’ll end up paying less in taxes. The level of tax relief you receive depends on your income and the tax rate applicable to you.

For example, if you are in the higher tax bracket and you contribute €100 to your private pension, you may receive €40 in tax relief, effectively reducing the cost of your contribution to €60.

This tax relief can significantly boost your retirement savings over time.

Furthermore, a private pension allows you to take control of your retirement savings, offering flexibility in investment choices and providing opportunities for your contributions to grow over the years.

How much should you save into your pension pot?

If you already have a pension, the exact amount to save for it depends on your unique situation and disposable income.

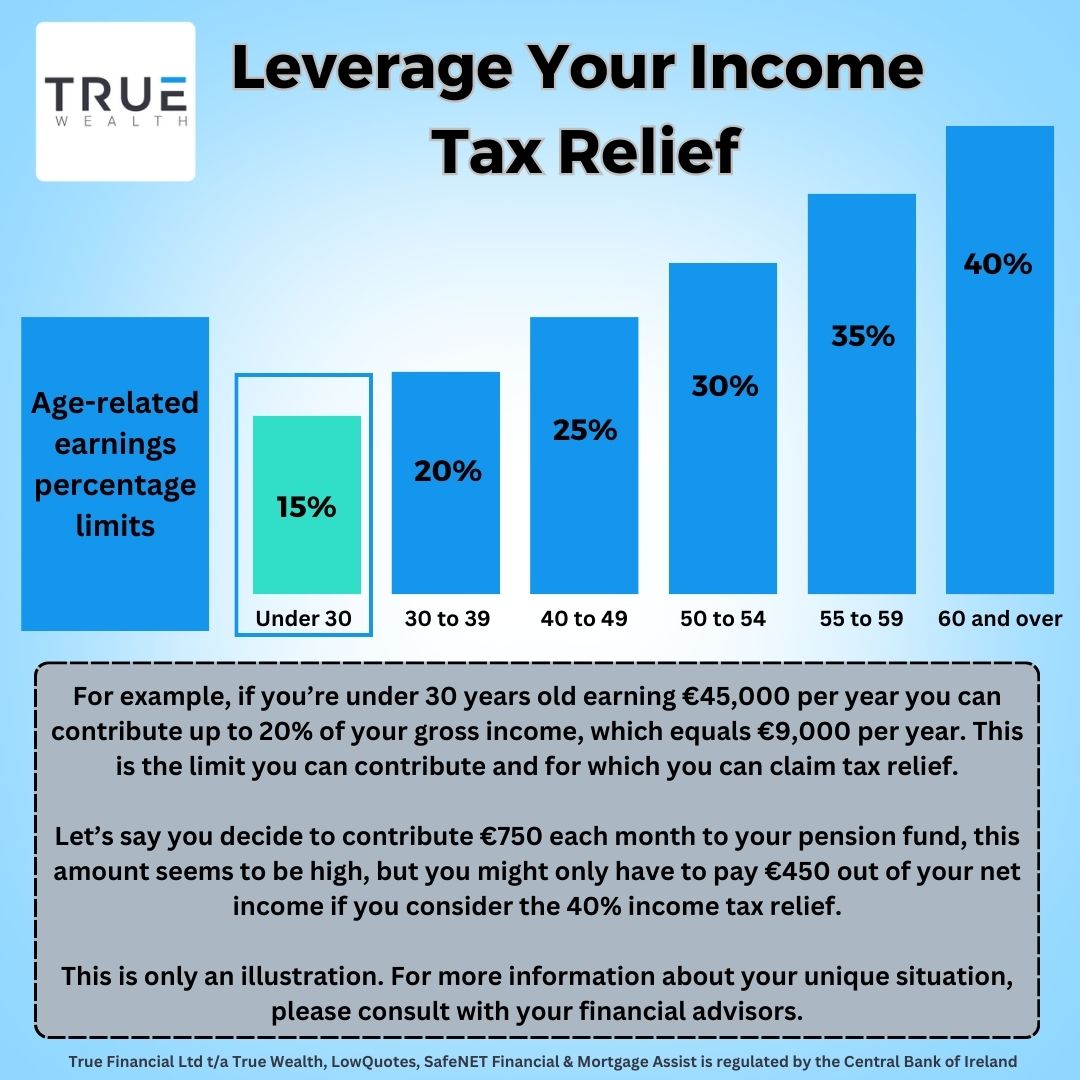

If you’re 20 years old, you can set aside up to 15% of your income for your pension and claim full tax relief. While this might seem like a lot, tax relief can make it easier to manage.

For instance, you’re earning €45,000 per year and decide to contribute €750 each month to your pension fund. This amount seems to be high, but you might only have to pay €450 out of your net income if you consider the 40% income tax relief.

Navigating the world of pensions can be a complex task, especially when you’re in your 20s.

We understand that it’s not always easy to determine the right amount to contribute to your pension pot to secure your future. That’s where our expertise comes in.

True Wealth is here to provide tailored pension guidance – get a quote today.

5. Take advantage of your employer’s schemes

Taking advantage of your employer’s pension scheme in your 20s is a smart financial move that can set you on the path to a secure retirement.

Enrol in the scheme as soon as you’re eligible. Many employer schemes have a waiting period before you can join, so don’t delay once you’re eligible.

If your employer offers a pension plan with matching contributions, be sure to take full advantage of this opportunity.

Your employer’s contributions can significantly increase your retirement savings, essentially giving you free money for your retirement fund.

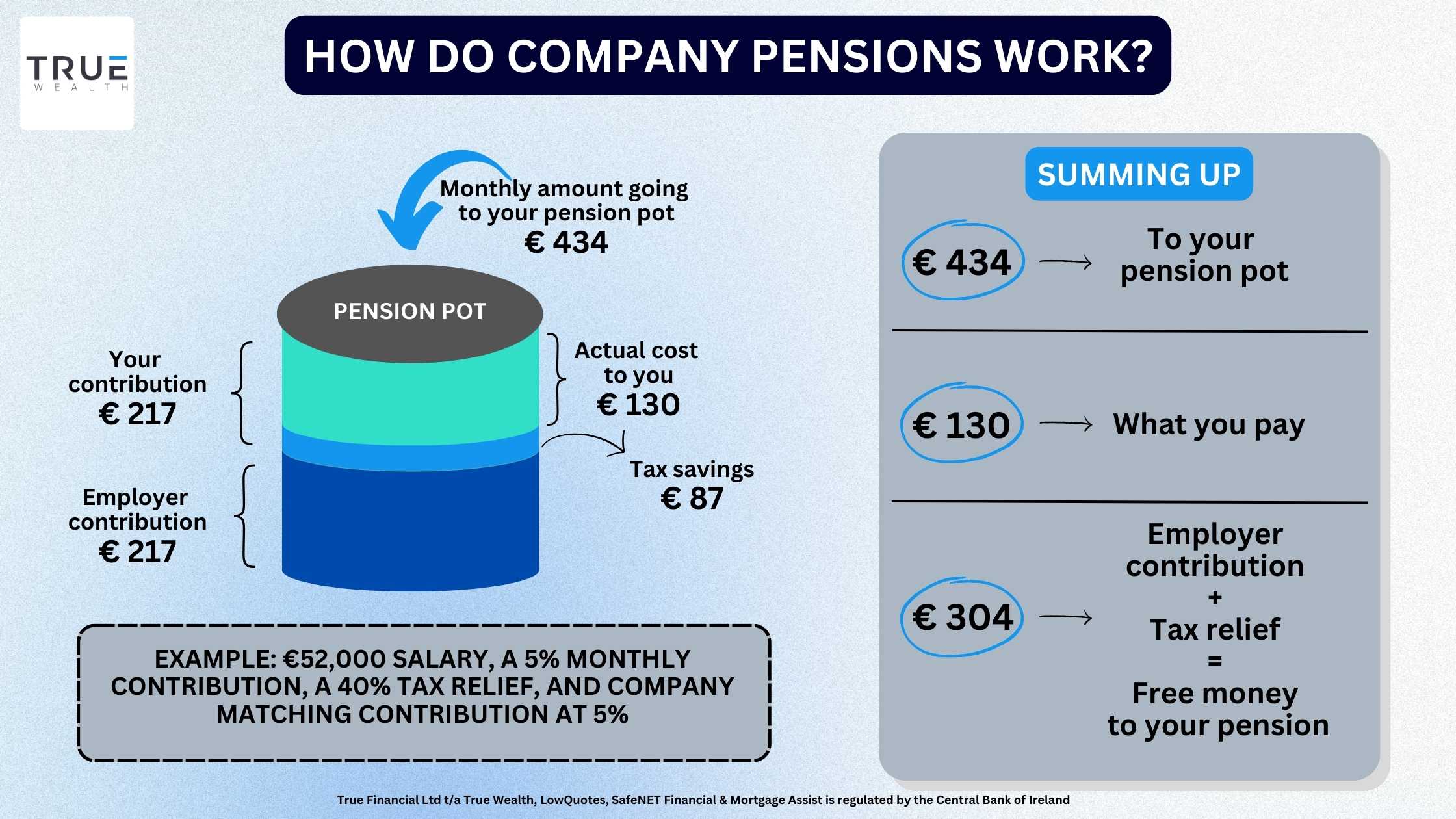

For example, consider a situation where you’re employed and are part of your company’s pension plan.

Your annual salary is €52,000, and you contribute 5% of your salary every month.

Your company matches your contribution at 5%. Additionally, your income places you in the 40% tax bracket.

Both you and your employer contribute €217 each, totaling €434.

What’s important to note here is that thanks to tax relief, your actual expense is only €130.

This means you can enhance your pension savings while spending less, all thanks to the tax relief benefit.

5. Understand Your Investment Options

Understand the investment options within your pension scheme.

You have choices on how your contributions are invested. Assess your risk tolerance and select investments that align with your retirement goals.

It’s always advisable to diversify your investments to spread risk and potentially increase your returns. Explore options like stocks, bonds, property, and other assets.

You can get professional guidance from our financial advisors at True Wealth.

6. Seek Professional Advice

Seeking professional advice in your 20s while planning for your retirement can be a game-changing decision that significantly enhances your financial security in later years.

We at True Wealth specialise in retirement and pension planning. We possess in-depth knowledge of various retirement investment options, tax strategies, and pension schemes.

Our expertise can help you make well-informed decisions tailored to your unique financial situation and goals.

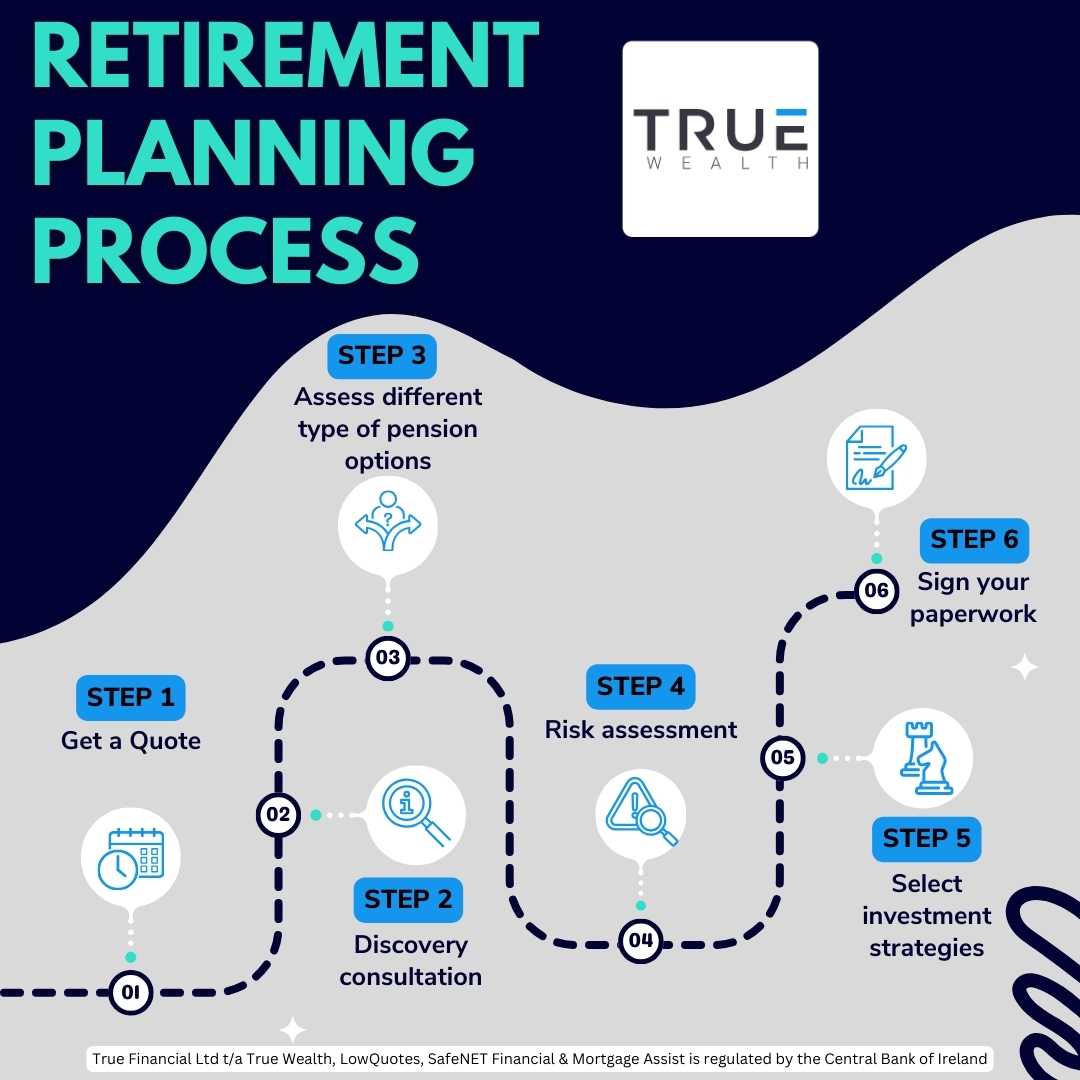

What is the Retirement Planning Process with True Wealth?

At True Wealth, we understand the importance of effective retirement planning and take pride in guiding our clients through each step of the process.

From the initial consultation to signing the paperwork, our dedicated team of financial advisors is with you every step of the way.

1. Get a quote

The first step in your Retirement Planning journey begins with getting a quote.

You will be asked some quick questions which will help us to pair you with a financial advisor to suit your unique situation.

2. Discovery consultation

During our discovery consultation, we provide you with your quote, and you’ll have the chance to have a one-on-one conversation with your dedicated financial advisor.

Your advisor will invest the time to grasp your unique situation and expectations, setting a solid groundwork for your retirement strategy.

Crafting a custom retirement plan involves a comprehensive fact-finding process. This entails collecting data about your current financial position, your comfort level with risk, your preferred investment options, and the timeline for your retirement.

This step is pivotal in evaluating the appropriateness of various pension options.

3. Assess different types of pension options

Our team will present you with a range of pension options tailored to your specific needs.

We will explain the advantages and disadvantages of each, ensuring you have a clear understanding of your choices.

This comprehensive assessment helps you make an informed decision about your pension plan.

5. Risk Assessment

Understanding your risk tolerance is fundamental to the pension process.

We will work with you to assess your comfort level with different levels of risk.

This information will guide the development of an investment strategy that aligns with your preferences and goals.

Usually for individuals in their 20s, our recommendation typically leans towards a strategy with lower to moderate risk.

6. Select investment strategies

Based on the risk assessment and your long-term objectives, we will recommend investment strategies that maximise your retirement savings.

Whether you prefer a conservative approach, an aggressive strategy, or something in between, our goal is to create a diversified investment portfolio that suits your needs.

7. Sign your paperwork

Once you are satisfied with your retirement plan and investment strategy, it’s time to sign the necessary paperwork to put your retirement plan in action.

Our team will walk you through all documentation, ensuring that you understand each aspect of your pension arrangement.

Your Retirement in Your 20s with True Wealth

At True Wealth, we understand that retirement planning isn’t the same for everyone, especially when you’re in your 20s.

We’re here to collaborate with you, creating a customised strategy that matches your specific financial circumstances, the way you live, and what you want from your retirement.

This personalised method guarantees that your plan is perfectly crafted to match your expectations.

Seeking professional advice from True Wealth is an investment in your future.

Don’t limit your retirement to the State pension; partner with True Wealth for a well-structured and tailored retirement plan.

We are also experts in personal and business protection, savings and investments, pension tracing, personal and business financial planning, mortgages, and wealth extraction.

What is an Approved Retirement Fund (ARF)?