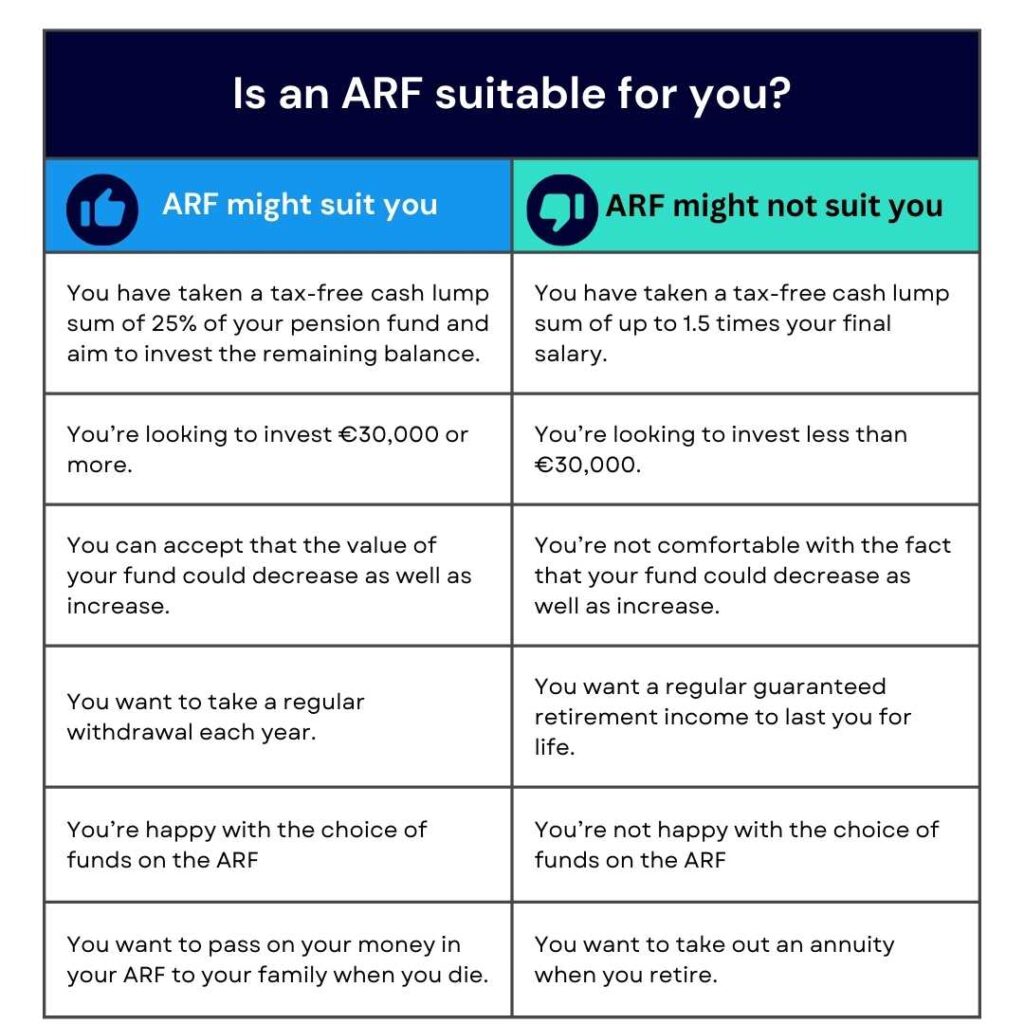

What is an Approved Retirement Fund (ARF)?

What happens with my ARF if I die?

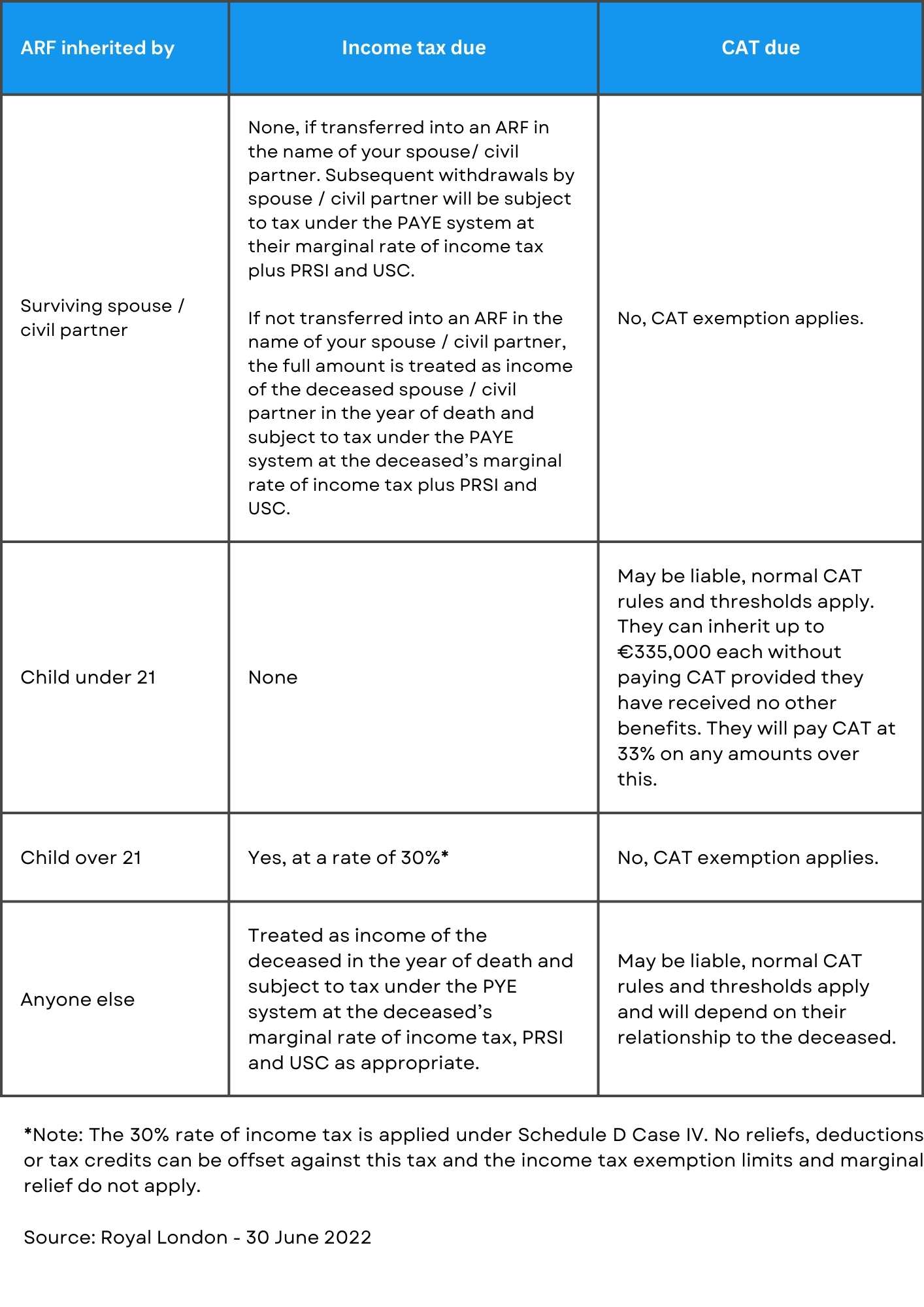

Payment on death

One of the main advantages of ARFs is that any money remaining in your ARF after your death can be left to your next of kin.

However, you need to specify in your Will that you want your ARF left to your spouse or other family members. Otherwise, your ARF will slide into the residue of your estate and it may not be distributed as you would like it to be.

How is your ARF taxed on death?

If your ARF is moved into an ARF under your spouse or civil partner’s name, there are presently no income tax or Capital Acquisitions Tax (CAT) obligations.

However, if you leave your ARF to another individual, they might be required to pay income tax and/or CAT, depending on their identity and, in certain cases, their age. If any income tax is due, it must be deducted before we release the ARF proceeds to your estate.

When planning your estate, it’s important to find ways to lower the inheritance taxes for your intended beneficiaries, as the tax rates can vary depending on who inherits the money.

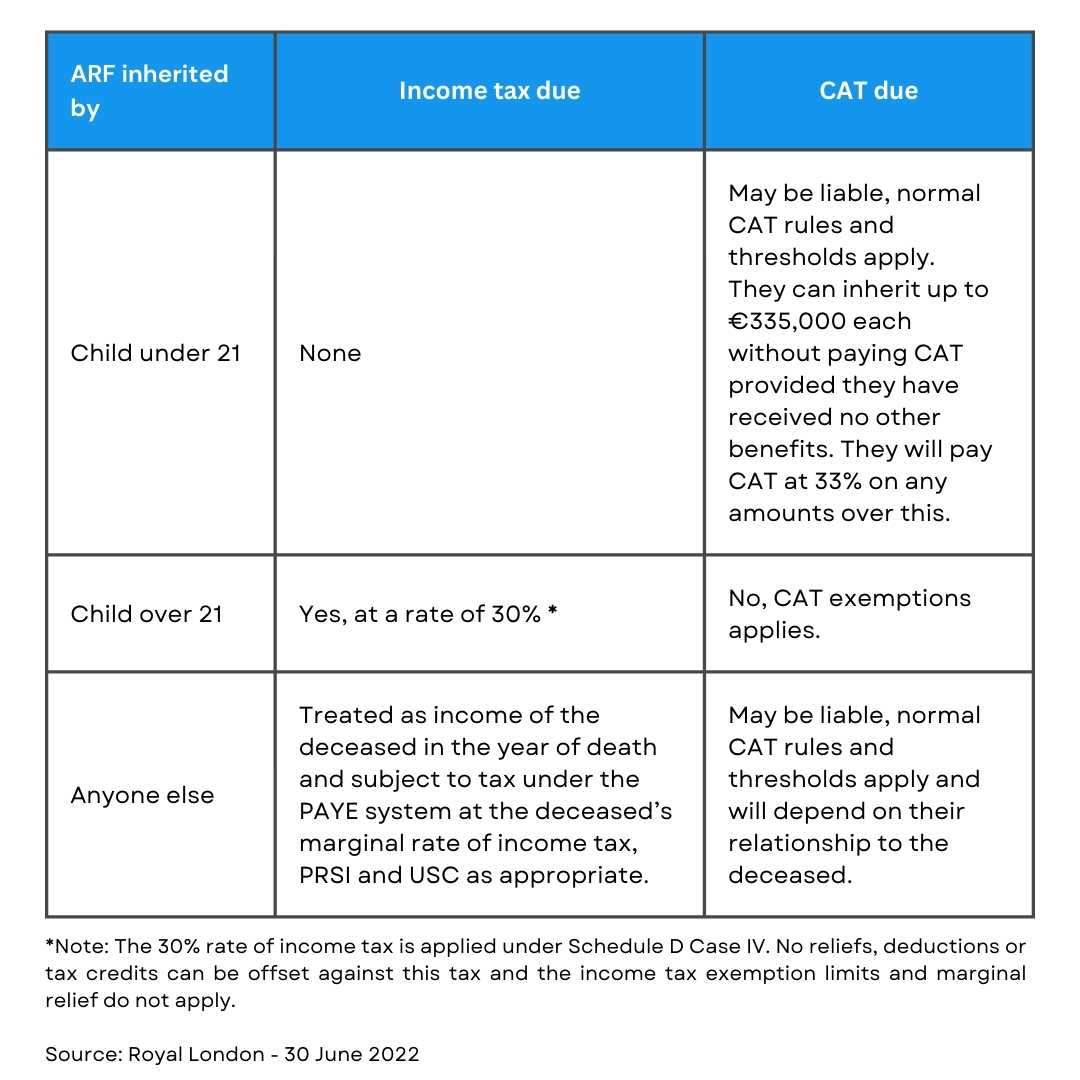

Summary of the tax rules after your death

Summary of the tax rules after the death of your surviving spouse/civil partner

If on your death, your ARF is transferred into an ARF in your spouse or civil partner’s name, the funds will be taxed on their death as follows:

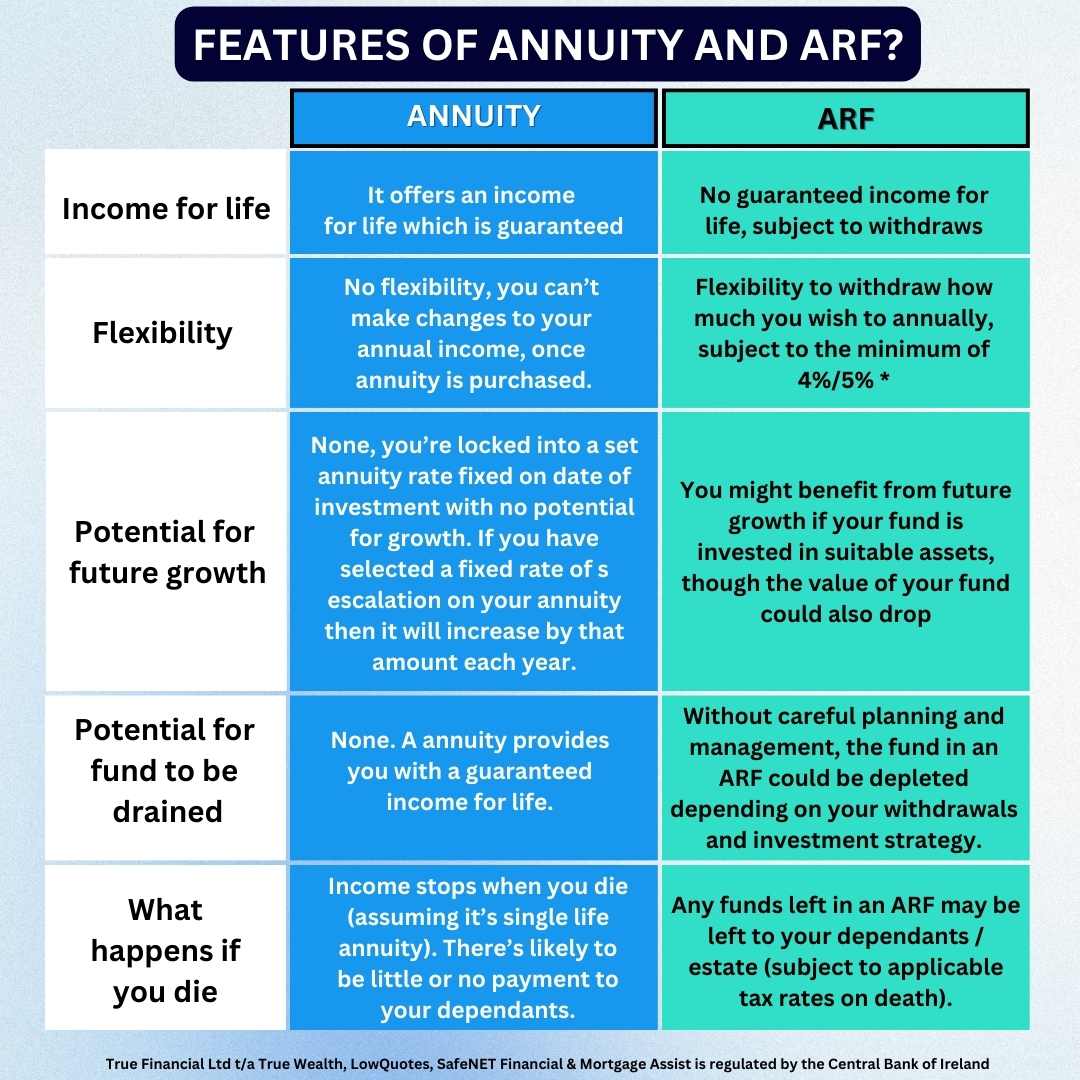

Which one is the best? Annuity or ARF?

The main difference is that with an annuity, the payment stops when the holder passes away, while with an ARF, the surviving spouse can inherit the money without paying taxes.

So, the decision is about whether you want a regular income or want to preserve the wealth for the future.

* Note:

- In the year an ARF policyholder turns 61, it’s compulsory to withdraw a minimum of 4% of the fund.

- In the year they turn 71 this increases to 5% per annum.

- If the ARF is greater than €2,000,000 then the minimum withdrawal is 6%.

How do you set up an ARF?

Setting up an ARF involves several steps, but it’s a straightforward process as we provide guidance at every stage.

- First, you must meet the eligibility criteria set by your pension plan and provider. Once you qualify, you’ll need to move your pension savings into an ARF account. This transfer can be done through your pension provider or a financial institution offering ARF accounts.

- Afterward, you can decide on how to invest your funds and manage your withdrawals. It’s crucial to collaborate with your dedicated financial advisor at True Wealth to make well-informed choices and maximise your retirement savings.

- To set up an Approved Retirement Fund (ARF), you’ll typically need to provide the following documents:

- Proof of identity (such as a Passport or Driver’s License).

- Bank details, including IBAN and Bank Identifier Code (BIC) for ARF withdrawals.

- Information about the source of your investment – where the funds for the ARF are originating from, which must be a pension product along with the policy, proposal, and plan number of your pre-retirement product (e.g., PRSA, PRB).

- Your attitude toward risk – this information will help in selecting suitable funds for your ARF.

Set up your ARF with True Wealth

Embark on your journey to establish your ARF with True Wealth.

Our experienced team specialises in retirement planning, and we are here to assist you every step of the way, making the process simple and ensuring your financial future is in capable hands.

We are also experts in personal and business protection, savings and investments, pension tracing, personal and business financial planning, mortgages, and wealth extraction.

Get in touch with us today to kickstart your ARF setup and secure your retirement plans.

Pension Annuities: Retirement Income For Your Whole Life