How High Earners Can Reduce Their Tax Bill Through Smart Planning

Table of Contents

If you’re earning a high income in Ireland, you’re likely paying a substantial portion of it in tax, sometimes over 50% when you include income tax, USC, and PRSI. And while paying tax is a reality of earning well, overpaying doesn’t have to be.

Many high earners are unaware of the full range of legal tax reliefs and planning strategies available to them. From maximising pension contributions and inheritance planning to tax strategies for business owners and using joint assessment effectively, there are smart ways to legitimately reduce your tax bill, both now and in the future.

Let’s take a look at who qualifies as a high earner, why tax planning is essential, and what you can do to protect your income and grow your long-term wealth.

Who Qualifies as a “High Earner” in Ireland?

The term “high earner” typically refers to individuals with an annual income exceeding €100,000, more than double Ireland’s national average income of approximately €50,000. However, the Revenue Commissioners use a more specific definition under the High Income Earner Restriction (HIER).

According to this rule, a person is considered a high earner if, in a given tax year, they have an adjusted income of €125,000 or more, claim specified reliefs of at least €80,000, and those reliefs amount to more than 20% of their adjusted income. These individuals are subject to restrictions on the amount of tax relief they can claim, to ensure that all high earners pay a minimum effective tax rate.

Why Tax Planning Matters for High Earners

Tax planning is a crucial component of your overall financial strategy. By proactively managing your taxes in conjunction with your income, pensions, investments, and long-term goals, you can significantly enhance your financial outcomes.

For high earners, tax planning is not just beneficial; it’s essential. As your income rises, so does the percentage taken in tax, with many high earners handing over more than 50% of their earnings through income tax, USC, and PRSI. Without a well-planned tax strategy, a significant portion of your income could be lost unnecessarily.

Effective tax planning enables high earners to legally and efficiently reduce their tax burden by utilising available relief, such as pension contributions, the Employment Investment Incentive Scheme (EIIS), and company pension funding. These options not only lower immediate tax bills but also support long-term financial goals such as retirement planning and wealth preservation.

With the right guidance, tax planning becomes a powerful tool for retaining more income and strengthening long-term financial security.

Get a Personal Financial Planning Quote

Here are a few ways tax planning can help you keep more of what you earn:

Joint Assessment (if married/civil partnered)

High earners who are married or in a civil partnership can significantly reduce their tax bill by selecting the most suitable assessment option. Under joint assessment, the income of both partners is combined and taxed as a single unit, allowing for a more effective use of the standard tax rate band and tax credits. This can be especially beneficial if one partner earns significantly more than the other.

Maximise Pension Contributions

One of the most powerful tax relief tools available is your pension.

Personal Pensions & PRSAs

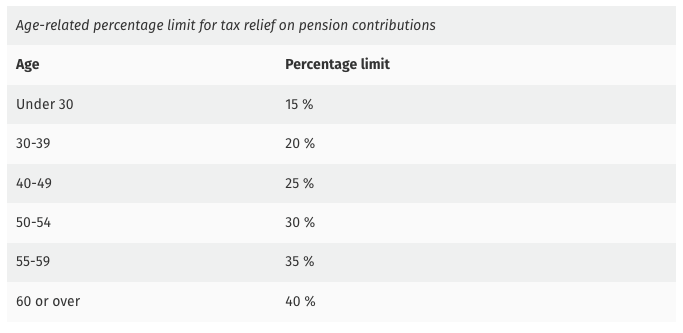

High earners can claim income tax relief on personal pension and Personal Retirement Savings Account (PRSA) contributions, but how much you can contribute and claim relief on depends on your age and earnings.

Here’s how it works:

- You can contribute a percentage of your earnings and claim income tax relief at your highest rate (up to 40%).

- The maximum earnings limit for calculating this tax relief in 2025 is €115,000.

- The allowed percentage depends on your age:

Example:

If you’re 47 and earn €115,000, you can contribute up to €28,750 to your pension and receive up to €11,500 back in income tax relief.

This is one of the most effective ways high earners can reduce their tax bill while building long-term wealth.

Company Directors: Extract Profits Tax-Efficiently Through Pensions

If you’re a company director, one of the most powerful ways to reduce your tax bill and build long-term wealth is through employer pension contributions. Unlike salary or dividends, pension contributions offer several unique advantages.

No Benefit-in-Kind (BIK)

When your company contributes to your pension, it’s not treated as a BIK, meaning you don’t pay any personal tax on it. It’s a legitimate business expense.

No Employer PRSI

Pension contributions made by your company are not subject to employer PRSI, which applies to regular salary payments at a rate of 11.15%, rising to 11.25% from October 2025. This makes pension contributions a more efficient way to extract profits and retain more within the business or pension fund.

No Income Tax, USC, or PRSI (until you draw down in retirement)

Unlike salary or dividends, pension contributions are not taxed as income until you retire and begin drawing them down, often when you’re in a lower tax bracket, significantly reducing the overall tax you’ll pay.

No Capital Gains Tax on investment growth inside the pension

Any growth within your pension, whether from stocks, funds, or property, is entirely exempt from Capital Gains Tax, allowing your investments to compound more effectively over time.

No Corporation Tax on the profits transferred into your pension

When your company contributes to your pension, those amounts are treated as business expenses and reduce your taxable profits, meaning you pay less corporation tax while funding your retirement.

Tax-free growth inside your pension fund

All earnings within your pension, including interest, dividends, and capital growth, accumulate without any tax deductions, allowing your retirement fund to grow faster compared to personal savings.

25% tax-free lump sum available at retirement (up to €200,000)

When you retire, you can take up to 25% of your pension fund as a tax-free lump sum, with a lifetime cap of €200,000, providing a valuable and tax-efficient source of cash at a time when you may want to travel, pay off debts, or support your family.

You can learn more by reading our Guide for Business Owners on Protecting, Extracting, and Growing Wealth in Ireland.

Get a Personal Financial Planning Quote

Invest Tax-Efficiently

For high earners, investing tax efficiently is key to preserving and growing your wealth. While traditional investments may expose you to income tax, capital gains tax, or DIRT, some options can reduce your tax burden.

Employment and Investment Incentive Scheme (EIIS)

The Employment and Investment Incentive Scheme (EIIS) allows you to invest in qualifying Irish businesses and claim up to 40% income tax relief on amounts up to €500,000 per year.

Pension Investments

Pension investments grow entirely tax-free until retirement, making them one of the most efficient vehicles for long-term growth. Structuring your investments through these approved schemes not only helps lower your annual tax bill but also maximises the net returns on your capital.

Approved Retirement Funds (ARFs)

After retirement, transferring your pension savings into an Approved Retirement Fund (ARF) gives you flexibility and control over how and when you access your money. One of the biggest advantages of an ARF is tax-deferred growth; your investments continue to grow free from income tax, DIRT, or capital gains tax.

You only pay income tax on the amounts you withdraw, which means you can plan your drawdowns strategically to stay in a lower tax bracket, particularly if your overall income decreases in retirement. This makes ARFs a powerful tool for high earners who want to manage their retirement income efficiently and preserve more of their wealth.

Corporate Investing for High Earners

High earners who own limited companies can benefit from corporate investing, which is one of the most tax-efficient ways to invest in Ireland, through a company. Corporate investments are subject to an exit tax of 25% on gains or interest income, significantly lower than the 41% tax rate individuals typically pay on most mutual fund returns. This enables company owners to accumulate wealth more efficiently within their business structure.

Learn more by reading our article: Corporate investments: Can you invest money from your company?

Inheritance Tax Planning for High Earners

For high earners, inheritance tax (Capital Acquisitions Tax or CAT) planning is essential to protect family wealth and ensure that more of your assets go to your loved ones, rather than to the Revenue. One key tool is the Annual Small Gift Exemption, which allows you to gift up to €3,000 per person per year tax-free, with no limit on the number of recipients. Over time, this lets you pass on substantial wealth while keeping it outside the scope of CAT.

You can also reduce inheritance tax by transferring assets during your lifetime, especially if done gradually. And if you’re a parent, there are smart ways to protect children from future CAT bills, especially when combined with the Group A threshold (€400,000 per child as of 2025). Planning ahead is essential if you own property or business assets that might otherwise trigger large tax bills.

Cohabiting couples face even greater risks than married couples or civil partners, who fall under the lowest CAT threshold. Without proper planning, the surviving partner could face a significant tax bill when inheriting a shared home or assets. Using tools like a life insurance policy under Section 72 can help reduce the tax burden and protect the surviving partner from financial strain.

Income Splitting (for Business Owners)

If you’re running a business, consider employing your spouse or adult children (if they do legitimate work). This can help spread income and reduce your personal tax load. Just ensure that payments are reasonable and well-documented.

Get a Personal Financial Planning Quote

Get a Financial Planning Quote

Paying tax is unavoidable, but overpaying doesn’t have to be. With the right financial strategies, you can significantly reduce your tax bill while growing and protecting your wealth over time.

Our experienced financial advisors can build a personalised financial plan that includes tax planning, helping you reduce your tax bill, grow your wealth, and protect your assets. Whether you’re looking to maximise pension contributions, plan for retirement, invest tax efficiently, or pass on wealth to your family, we’ll guide you every step of the way. Let us help you make your money work harder — and smarter — for you.

We are experts in personal and business protection, savings and investments, pension tracing, retirement planning & pensions, business owner and personal financial planning, mortgages, and wealth management and extraction.

Share this post.

All our content has been written or overseen by a qualified financial advisor. However, you should always seek individual financial advice for your unique circumstances.

Warning: Past performance is not a reliable guide to future performance.

Warning: The value of your investment may go down and up.

Warning: If you invest in this product, you will not have any access to your money until you retire.

Warning: If you invest in this product, you may lose some or all of your investment.

Warning: This product may be affected by changes in currency exchange rates.

Strategic Wealth Extraction for Business Owners’ Future