Understand Personal Retirement Savings Accounts (PRSAs)

{kind=link}

How can I check the performance of my PRSA?

Every year (or every six months, depending on the provider), you’ll receive a pension statement from the provider.

This statement will detail the contributions made to your PRSA and an investment report showing the returns earned on the funds.

The annual pension statement also includes a projection of potential future benefits you could receive upon retirement. This projection is based on the current value of your PRSA, expected future contributions, prevailing charges, and assumed rates of investment growth.

Can I transfer to and from my PRSA?

Yes, transferring your pension to and from your PRSA is possible, provided that legislative requirements are met.

Transfers into your PRSA

Your PRSA can accept transfers from various sources, including another PRSA, an Occupational Pension Plan, a Retirement Annuity Contract (Personal Pension Plan), refunds of contributions from an occupational pension scheme, and pension arrangements outside the State.

Usually, there are no initial charges imposed on transfers received into any of our PRSA products.

Transfers from your PRSA

If you decide to transfer your accumulated fund to another pension arrangement, several types of pensions may accept transfers from your PRSA, including another PRSA, an Occupational Pension Plan, and pension arrangements outside the State.

Key Benefits of Personal Retirement Savings Accounts (PRSAs)

Tax Deductible Contributions

One of the primary advantages of PRSAs is the tax benefits they offer. Contributions made to a PRSA are typically tax-deductible, meaning you can reduce your taxable income by contributing to your retirement savings.

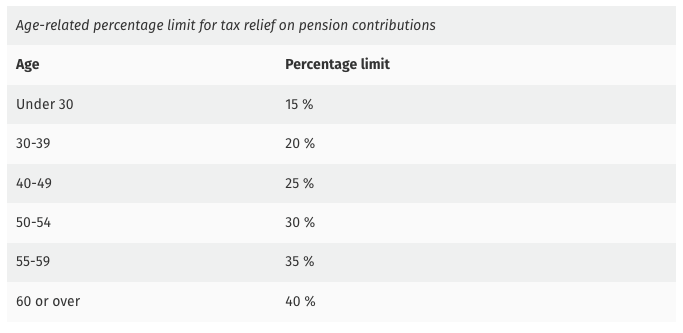

Contribution amount qualifying for tax deduction

The tax relief for pension contributions has two primary limitations: an age-related earnings percentage limit and a total earnings limit.

You can receive tax relief up to the applicable age-related percentage limit of your earnings within a given year.

For example, if you’re 29 years old, to avail of tax relief, there’s a limit of 15% of your total income that can be allocated to your pension fund.

As you move through the age groups, this allocation limit gradually increases until it reaches its maximum at age 60 and beyond, at which point it stands at 40% of your salary.

The maximum annual earnings taken into account for calculating tax relief is €115,000.

Note that employer contributions to an employee’s pension scheme do not influence the calculation of the employee’s earnings threshold.

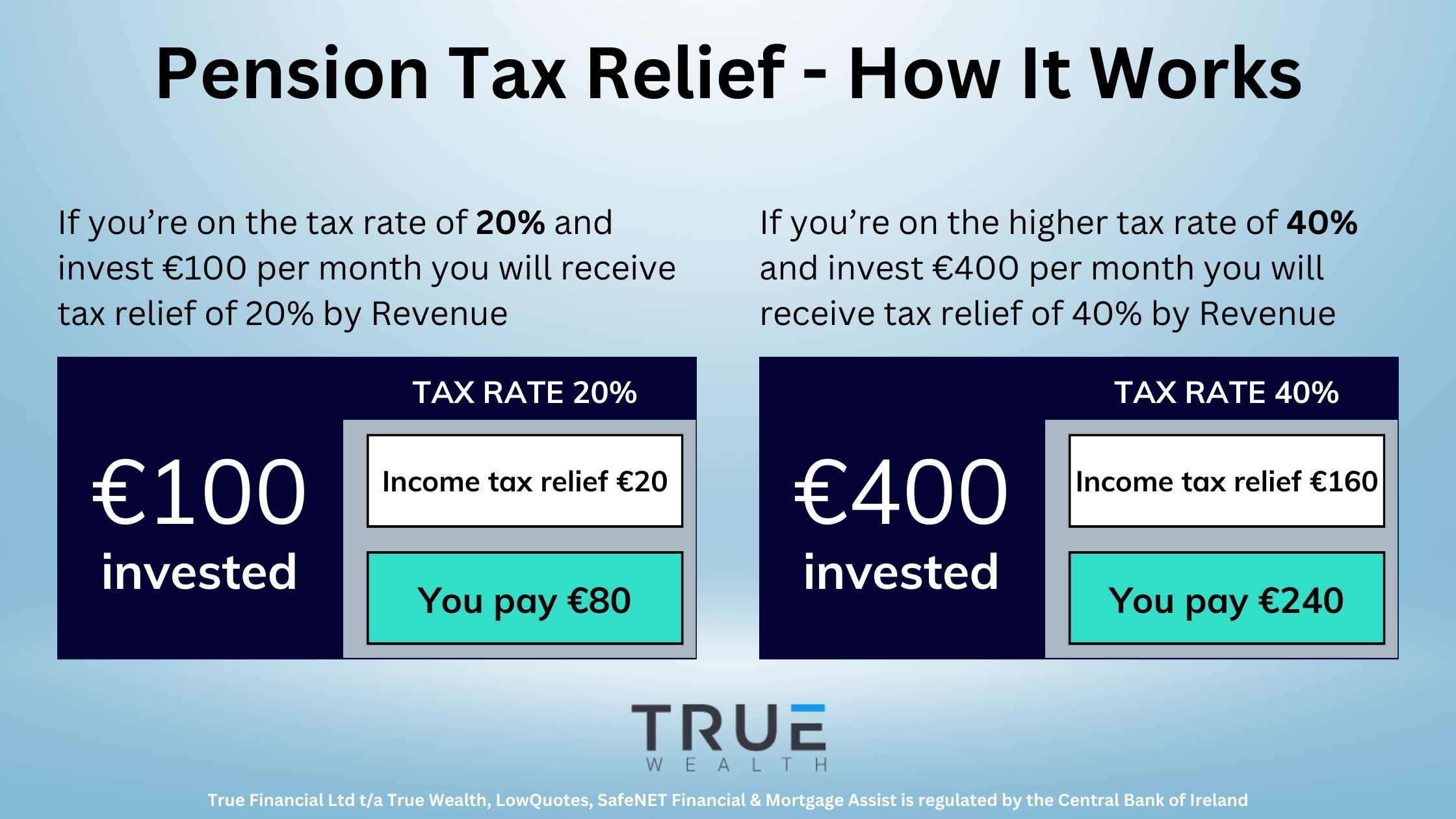

How tax relief works

If you contribute to a pension plan, you are eligible to receive income tax relief on your contributions.

The maximum income tax rate that applies to you, also known as the marginal rate, determines the amount of tax relief on your pension payments.

The exact benefits and rules can vary, so it’s advisable to consult with one of our financial advisors at True Wealth.

Alternatively, delve into our Retirement Guide to gain a comprehensive understanding of various aspects crucial for planning your retirement.

Tax-Free Investment Gains

Within a PRSA, any investment gains generated are not subject to taxation. This tax-free growth enables individuals to maximise the growth potential of their retirement savings.

Accessibility

PRSAs are accessible to everyone, regardless of their employment status. Whether you’re a full-time employee without a pension, self-employed or even taking a career break, you have the option to open a PRSA and start saving for retirement.

Flexibility

PRSAs offer flexibility in terms of contribution amounts. You can adjust your contributions according to your financial circumstances, increasing, decreasing, or even stopping contributions altogether without incurring penalties.

Portability

Another key benefit of PRSAs is their portability. You can carry your PRSA from one job to another or transfer it to a different PRSA provider without facing any charges or penalties.

This mobility ensures that you can maintain continuity in your retirement savings regardless of changes in employment.

To gain further insights into transitioning careers or changing jobs while maintaining your pension plan, we recommend reading our article, What Happens To Your Pension After Leaving Your Job?

Retirement Options

Upon reaching retirement, you have the option to withdraw a tax-free lump sum equivalent to 25% of your fund, capped at a maximum of €200,000.

Subsequently, the remaining portion of your fund can be allocated towards either an Annuity or an Approved Retirement Fund (ARF).

If you set up a PRSA for making Additional Voluntary Contributions, it’s important to note that you must access your benefits from the PRSA the same way you get benefits from the primary scheme.

Get your retirement and planning quote with True Wealth

Whether you’re considering setting up a PRSA or seeking expert advice on retirement strategies, we’re here to help you make informed decisions and achieve your financial goals.

Trust True Wealth to provide personalised solutions tailored to your unique circumstances, ensuring a secure and prosperous retirement ahead.

Gain valuable insights by exploring our Retirement Planning Guide, offering comprehensive knowledge to help you navigate the intricacies of retirement planning and pensions.

We are also experts in personal and business protection, savings and investments, pension tracing, personal and business financial planning, mortgages, and wealth management and extraction.

Tax-Free Gift for Mortgage: Support Your Child’s Homeownership