What Are the Differences Between a State Pension and a Private Pension?

Why Should I Have a Private Pension When There’s a State Pension?

The state pension in Ireland is a valuable source of income for retirees. However, it might not be enough to maintain the lifestyle you desire during retirement.

With the state pension currently at €277.30 per week (as of January 2024), it’s crucial to consider the bills and expenses you’ll likely face and assess if this amount will be adequate for your financial well-being. If the answer is no, a private pension becomes an essential financial tool for securing your future.

A private pension can provide an additional income stream to cover living expenses, healthcare, mortgages, children’s education and leisure activities.

Relying solely on the state pension might not be enough to sustain you, making it important to have another pension arrangement in place to support you when you retire.

Discover more by reading our article on the benefits of having a private pension.

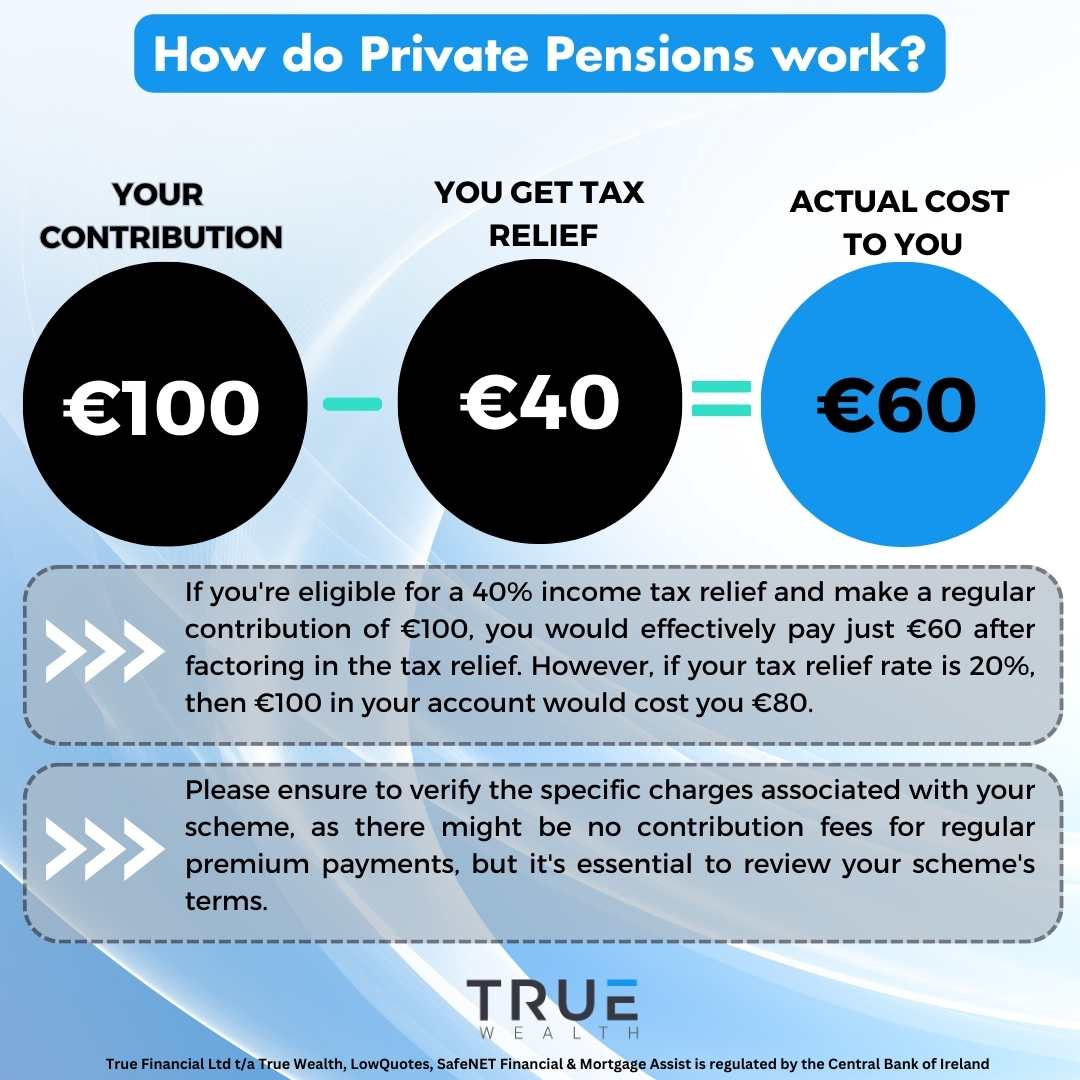

How do pensions work?

When you contribute to your private pension, the government provides tax relief, which means your contributions are deducted from your taxable income. The level of tax relief depends on your income and tax rate.

For example, if you’re in the higher tax bracket and contribute €1,000, you may receive €400 in tax relief, reducing your effective cost to €600. This tax relief can significantly enhance your retirement savings over time.

Additionally, a private pension offers flexibility in investment choices, allowing you to tailor your plan to your financial goals and risk tolerance. Explore our retirement guide for more information.

Is Auto-Enrolment the Best Option for Your Business?